Sensitivity analysis is a good technique for forecasting the attention of management on critical variable and showing where additional analysis may be beneficial before finally accepting a project. It does not directly measure risk and it is limited by only being able to examine the effect of a change in one variable, while the others remaining constant, an unlikely occurrence in practice.

Sensitivity analysis enables investigation into how projected performance will vary along with changes in the key assumptions on which capital project projections are based. The NPV of a project is based upon the series of cash flows and the discount factor. Both these determinants depend upon so many variables such as sales revenue, input cost, competition etc.

Given the level of all these variables, there will be a series of cash flows and there will be NPV of the proposal. If any of these variables changes, the value of NPV will also change. It means that the value of NPV is sensitive to all these variables.

The sensitivity of a capital budgeting proposal, in general, may be analyzed with reference to:

1. Level of revenues

2. Operating margin

3. Expected growth rate in revenues

4. Working capital requirements as a % of revenue etc.

Sensitivity Analysis helps in identifying the different variables having effect on the NPV of a proposal. It helps in establishing the sensitivity or vulnerability of the proposal to a given variable and showing areas where additional analysis maybe undertaken before a proposal is finally selected.

The final decision on whether or not to take up the proposal will be based on regular budgeting analysis and the information generated by the sensitivity analysis. Sensitivity analysis is one of the objective methods to ascertain the impact on final probability by taking specific changes in each critical factor or variable.

Thus, if a company is to operate in a highly competitive market, with many rivals, sales volumes and price will be critical variables and hence, one would like to assess how sensitive the project is to changes in sales volume or price.

Sensitivity analysis seeks to determine the range of variations in the coefficients over which the solution will remain optimal. Sensitivity analysis is used in determination of risk factor in capital budgeting decisions. It aids in identifying the most sensitive factor that may cause the error in estimation. Sensitivity analysis tells about the responsiveness of each factor on the project’s NPV or IRR.

For example, a 5% change in the selling price will cause 10% change on NPV, that means an increase of 5% in the selling price will increase 10% of the amount of NPV. Likewise, sensitivity analysis is done for all other factors like materials cost, labour cost, variable overhead, fixed overhead etc. Then, the most sensitive factor of all will be identified to evaluate the risk of that particular factor.

Sensitivity analysis involves the following three steps:

Step 1:

Identification of all those variables having influence on the project’s NPV or IRR.

Step 2:

Definition of the underlying quantitative relationship among the variables.

Step 3:

Analysis of the impact of the changes in each of the variables on the NPV of the project.

Advantages and Limitations of Sensitivity Analysis:

Advantages:

a. It gives greater visibility to the weak spots in an investment.

b. It will help management to more critically investigate such factors to validate the assumptions.

c. It aids management in proper decision-making.

Limitations:

i. Variables are often interdependent, which makes examining them each individually unrealistic. For example, change in selling price will effect change in sales volume.

ii. The analysis is based on using past data/experience which may not hold in future.

iii. Assigning a maximum and minimum or optimistic and pessimistic value is open to subjective interpretation and risk preference of the decision-maker.

iv. It is neither risk-measuring nor a risk-reducing technique. It does not produce any clearer decision rule.

Problem:

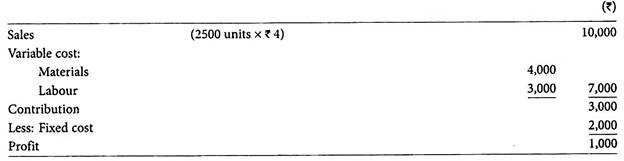

Premier Industries Ltd. Has prepared the following budgeted profitability statement for the current year operations:

Make a sensitivity analysis based on the above data.

Solution:

The changes in the sales revenue and costs on profit can be analyzed with the help of sensitivity analysis as follows:

(a) If selling price is reduced by more than 10% budgeted, the company would incur loss.

(b) If the sales are reduced by more than 10% of the budgeted sales of 2500 units, the company would incur loss.

(c) If labour costs increase by more than 33.33% above the budgeted, the company would make a loss.

(d) If material cost increases by 25% or more of the budgeted cost, the company would make a loss.

(e) If the fixed costs increase by more than 50% of budgeted fixed cost, the company would incur loss.

If we observe the sensitivity of the above data, sales units and selling price per unit is more sensitive than other items of cost. Hence this area remain careful consideration.