This article throws light upon the five main management exercises before taking final decision on farm. The management exercises are: 1. Appraisal of Farm Resources 2. Appraisal of Land Resources 3. Appraisal of Capital Resources 4. Entrepreneurial Appraisal.

Management Exercise # 1. Appraisal of Farm Resources:

The basic aim on commercial farms are the minimization of cost and maximization of profit. The farm resources comprises of land, labour, capital, organization and enterprise (bearing risk and reaping benefit or sustaining loss.)

The land is the primary factor of production and is passive in nature which needs it exploitation—in the sense of using them in most judicious manner—The land is limited in quantity and varies in quality in most of the farm with the exception of a few farms where there may be homogeneity in terms of physical, chemical and biological characteristics.

Thus, it shows that qualitatively the land varies physically, chemically and biologically.

ADVERTISEMENTS:

The labour in underdeveloped country, India as an example, is surplus and there is disguised unemployment. Indian fanners have been adjudged as the most efficient in the use of resources and hardworking but in general, the labour differ in their skill and efficiency. Indian farmers need scientific education.

Capital is the most scarce commodity on the farm. Indian farmers are said to be “not born with the silver spoon”, further it is said that an Indian farmer is born in debt, lives in debt and leaves behind debt for his progeny to continue in the same fate. Capital shortages will tell upon the efficiency and productivity.

With the nationalization of banking institution it is claimed that borrowing is not that big a problem for the Indian farmers particularly those who belong to socially weaker sections of the society. There have been many commissions to enquire into the functioning of the banking institutions and they have reported weakness in the system.

The organization of the farm is reflected in the efficiency in the use of resources which is measured in terms of productivity of the three major factors of production viz., the land, labour and capital.

ADVERTISEMENTS:

The Royal Commission on agriculture has appreciated the organizational efficiency of the Indian farmer in the utilization of their resources. They recommended the education of the farmers in latest method of scientific agriculture.

The entrepreneurship of the farmers is put to test when they adopts the latest technology. Many studies have been conducted in this direction to find out which category of farmers do adopt the technology when made available to them and who are the early adopters. This very much depends on the factors like education, age and social level etc.

Management Exercise # 2. Appraisal of Land Resources:

Appraisal is the determination of value to a resource. The value of the land is judged by its productivity which may be due to its original (inherent) quality or by its management in the past.

The relative value of land depends on:

ADVERTISEMENTS:

a. Climatic condition,

b. Type of soil,

c. Nature of surface soil and sub-soil,

d. Depth of soil and its composition,

ADVERTISEMENTS:

e. The ground water table,

f. Size and shape of land,

g. Slope of the land,

h. Sunshine and shadow,

ADVERTISEMENTS:

i. Past use of land,

j. Distance from the farmstead,

k. Type of road reaching the fields,

l. Distance of the farm from the market.

ADVERTISEMENTS:

The physical properties of soils are: its texture and structure, colour of the soil, porosity of the soil, its organic matter content, water holding capacity, slope for determining the soil erosion, soil temperature etc.

The chemical properties are: the soil reaction—acidic or alkaline soil, mineral content, soil forming rocks.

The biological properties of soil depend on the nature of microorganism present in the soil-useful or harmful micro-organism, extent of pollution due to its use in the past.

The criteria for land valuation are:

ADVERTISEMENTS:

(a) Market value of gross produce of the land,

(b) Market value of the net product (income) from the land,

(c) Sale value of land,

(d) Capitalizing the rent of the land.

We are discussing the Income Capitalization Method: This depends on annual net income from the land, prevailing rate of bank interest, i.e., on long term investment or capitalization rate.

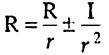

The formula: V = R/r

ADVERTISEMENTS:

where, V = Capitalized value of land; R = the net income or return per year; r = rate of interest. This formula is applicable in case where the income is constant.

In case of variable income (rising or falling) a corrective factor is put:

where, I = the increase or decrease in income.

Valuation of Labour:

India is a labour surplus economy because of the population due to large family sizes.

ADVERTISEMENTS:

The sources of labour on the farm are:

i. Family Labour:

Farmer and his family both male and female.

ii. Hired Labour:

It may be a permanent labour which works for the farmer regularly for a salary or some other benefit like land given to him. The other is the casual labour which the farm owner employs from time to time on daily wages in cash of kind.

The farm labour may be further classified as: Skilled labour—which is trained for a certain job like tractor driver; Unskilled—which has no special, training.

ADVERTISEMENTS:

The efficiency of labour is a two dimensional entity:

(a) The inherent quality of labour himself;

(b) The ingenuity of the farm manager in making use of the labour i.e., how does the farm manager organizes the work on the farm.

It is not the quantity of labour but its quality which increases the labour productivity and output.

The measure of efficiency of labour is through productivity per unit.

The other measures of labour efficiency are:

ADVERTISEMENTS:

i. Crop per acre per person,

ii. Net livestock production per person,

iii. Gross profit per person,

iv. Productive man-work unit per man.

These work efficiency measures are taken into consideration while preparing a farm plan and preparing the budget for the farm—which is income and expenditure account for the accounting year.

Management Exercise # 3. Appraisal of Capital Resources:

Capital comprises of both tangible commodity as well as intangible one. Capital thus becomes an input in farming activity such as seed, fertilizer, plant protection chemicals, machinery and equipment’s and the technology used in productive activity.

ADVERTISEMENTS:

The knowledge of scientific and technological application is also known as human capital. Capital, therefore, can be defined as a factor of production that generates the flow of income spread over a certain period of time.

Capital used in farming comprises of:

(a) Fixed capital—which is used time and again, its examples are found in farm machinery and equipment and farm buildings. The depreciation and interest due to these assets is known as fixed cost.

(b) Variable capital—this is used once for all and its quantity varies with the output. Examples, of these are found in seeds, fertilizers, plant protection chemicals and wages paid out to hired labour.

The capitals used in farming activities are given valuation by the following three methods:

(a) Market value—the price of the capital assets at the current market price,

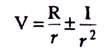

(b) Capitalization of the anticipated income—the formula used is: V = R/r (for constant return)

(this is used for fluctuating incomes),

(c) The initial price of the asset minus or plus its depreciation or appreciation. This will be the value of the asset in year following.

There are six methods of calculating depreciation:

(i) Straight line method,

(ii) Diminishing balance method,

(iii) Sum of the years digit,

(iv) Depreciation or Sinking fund method,

(v) Annuity system,

(vi) Revaluation method.

Capital Efficiency are Measured:

(a) Input-output ratio both in physical and value terms.

(b) Quantity or value of crop products or livestock products per unit of capital input used, viz., fertilizer feed or per rupee investment.

(c) Quantity or value of livestock products per unit weight or value of feed consumed.

(d) Crop acreage per tractor.

(e) Rate of capital turnover.

(f) Power, machinery, equipment expenses per productive man-work unit.

Management Exercise # 4. Appraisal of Management Factor:

To evaluate management is not an easy task but there are two indexes which reflect the managerial efficiency, they are:

(a) Efficiency,

(b) Capacity.

Efficiency is the input-output ratio and is measured in:

i. Crop yield as a percentage of average yield from similar soil.

ii. Return per Rs. 100 worth fed to livestock (according to class.)

iii. Percentage of normal power of machinery cost,

iv. Percentage of return from normal labour cost.

Capacity is adjudged as a farm manager maintaining his efficiency could handle more or additional operations or business.

Management Exercise # 5. Entrepreneurial Appraisal:

Generally, the farm organizer and the entrepreneur (owner) is the one and the same person. If the entrepreneur enter a new enterprise which seems to him promising in his business endeavour and it goes very well as per his aspirations he reaps the profit or if the enterprise does not give expected results the entrepreneur sustains the losses.

In the agricultural business risks are broadly classed as:

(a) Personal Risk:

These risks are to outsiders or third party and also risk to farmer and farm worker.

The nature of such risks would be:

(i) Economic—inability to sell the labour power or unemployment,

(ii) Social—accidents or employers liabilities,

(iii) Natural—old age, sickness, maternity for women farm workers.

(b) Property Risk:

These may again be economic, social and natural. Economic risks are fluctuation of prices, un-expected-lessness, changes in prices of farm inputs, Social—civil disturbances, strikes, change in social trend. Technological change— Natural risks—plant and animal diseases, rodent, insect-pests, pollution.

Averting Risks:

Risks in farming could be averted by several means, they are:

i. Avoid risks wherever the farmer could like selection of farm, and selection of enterprises.

ii. Prophylactic measures—application of plant protection chemicals without the appearance of diseases or pests but whenever there may be probability of such occurrences.

iii. To assume the risk:

(a) Insurance:

It is done against the probability of greater loss in crops or livestock, for example, in crops occurrence of blight, redrot and in animals rinder pest, foot and mouth diseases, at the nominal cost through insurance.

(b) Diversification:

Growing of variety of crops, in case one is lost the other may sustain the farmer from incurring greater losses. This minimizes the total loss.