Business has certain social objectives, besides the economic objectives. Business and culture are closely connected and they influence each other.

Social and cultural environment refers to the influence exercised by certain social and cultural factors like family, marriage, religion, education, attitude of people to work, ethics, attitude to wealth and social responsibility of business.

Business is an economic venture. Involving regular production and exchange of goods and services, it is carried with a clear intent to make money by offering essential and sometimes luxury goods and services to the customers.

Any business tries to create customers and help them get what they want in terms of variety price, quality, etc. The environment in which a business is carried out is very risky. You may have to fight competition; at times push your rivals against the wall.

ADVERTISEMENTS:

The term business is as old as civilisation itself. Business like any other human effort, either individual or joint is an activity.

The modern corporate bodies have evolved into a social as well as an economic institutions. They have concern and ideals and responsibilities which go far beyond the profit motive. Business is an assembly, not of brick and mortar but of human beings who have to be organised for “Joint Performance”.

Learn about: 1. Introduction and Meaning of Business 2. Concept of Business 3. Scope 4. Characteristics 5. Objectives 6. Classification 7. Diversification 8. Factors 9. Market Conditions for Creating a New Business 10. Role of Profit.

What is Business: Meaning, Concept, Scope, Characteristics, Objectives, Classification, Factors and Diversification

Contents:

- Introduction and Meaning of Business

- Concept of Business

- Scope of Business

- Characteristics of Business

- Objectives of Business

- Classification of Business

- Diversification of Business

- Factors of Business

- Market Conditions for Creating a New Business

- Role of Profit of Business

What is Business – Introduction and Meaning

Business has certain social objectives, besides the economic objectives. Business and culture are closely connected and they influence each other. Social and cultural environment refers to the influence exercised by certain social and cultural factors like family, marriage, religion, education, attitude of people to work, ethics, attitude to wealth and social responsibility of business.

ADVERTISEMENTS:

The cultural environment may influence the business in many ways, Government policies, legal environment, political system, labour-management relations, attitude of workers and business ethics could have a social influence on them. The culture of a society can directly affect management approaches and organisational behaviour. The tastes and preference, method of consumption, purpose and occasion of consumption, purpose of consumption etc. of a product may show wide differences between cultures.

The types of products to be manufactured, the methods of marketing of product, the organisation of business etc. are all influenced by social structure and culture of a society. Cultural difference is one of the most difficult problems in international business.

Literary meaning of business is the state of being busy. An individual being busy in some activity is the simple meaning of business. In the field of economics, business may be defined as any activity which leads to production of goods and or services to satisfy human needs and to earn reasonable profit.

ADVERTISEMENTS:

The term business is as old as civilisation itself. Business like any other human effort, either individual or joint is an activity. The modern corporate bodies have evolved into a social as well as an economic institutions. They have concern and ideals and responsibilities which go far beyond the profit motive. Business is an assembly, not of brick and mortar but of human beings who have to be organised for “Joint Performance”.

What is Business – Concept

Business is an economic venture. Involving regular production and exchange of goods and services, it is carried with a clear intent to make money by offering essential and sometimes luxury goods and services to the customers. Any business tries to create customers and help them get what they want in terms of variety price, quality, etc. The environment in which a business is carried out is very risky. You may have to fight competition; at times push your rivals against the wall.

At times, you may even have to sell below cost. Howsoever tough the environment could be, you have to serve customers quickly, efficiently, and effectively (remember McDonald’s). You must always strive to be better than the best in the field and be prepared to face the consequences whenever things go wrong. The path of business, in any case, is not a rosy one. Problems of various kinds may hit operations from time to time.

Let us examine these issues in greater detail:

ADVERTISEMENTS:

1. Sale, Transfer or Exchange of Goods and Services:

Any business involves sale, transfer or exchange of goods, and services for a price. The exchange process is undertaken with a view to making money. It is not done either out of charity or desire to help people or to meet personal ends.

2. Dealings in Goods and Services:

A business is created to primarily satisfy the others’ need for a particular goods or services. Customers generally buy those things that they want at various price points. It is for the businessman to find out what-the customer wants and make an attractive, mutually beneficial offer. Obviously, customers will not buy what you intend to sell unless they see value in the offer (top quality, economical price, discounts; price offs, concessions, etc.). Likewise, you cannot sell anything and everything and at every place. So, every businessman must choose well in advance what to sell, where to sell, how to sell, and at what price to sell.

ADVERTISEMENTS:

3. Regularity and Continuity in Dealings:

For any business, the show must go on forever. It is not a one-shot deal. A single transaction of selling a used car or buying a colour television cannot be called a business transaction. Businesses indulge in regular buying, selling, trading, exchanging of goods, and services on a continual basis. They are not one-time wonders.

4. Profit Motive:

Business is an economic activity. The ultimate goal is to make money by serving customers well, in the process, exhibiting ethical, moral and legally acceptable behaviour. If you want to make money quickly or earn a few dollars more by cutting corners here and there, you will be shown the door. The market ruthlessly punishes those who fail to live up to the expectations of the vast multitude of customers and society at large.

ADVERTISEMENTS:

5. Risk and Uncertainty:

Customers are notoriously fickle minded. Their tastes and preferences change in an unexpected manner. Business may face shortages in the supply of key inputs. Power breakdowns may happen, workers may go on strike, competition may get intense, cut-throat and high challenging, and the government may impose additional taxes suddenly. The future, thus, is full of uncertainties and turns our bets risky. A businessman might buy large quantities of sugar, wheat, rice, etc., in anticipation of festival demand.

The entire demand might vanish if the area is inundated with floods or hit by other natural calamities. An unexpected turn of events may bring in misery and cause incalculable damage. The impact could prove to be suicidal and the business may be wiped out completely. A businessman must, therefore, be prepared to face the music from any place and any corner. Business ventures may turn out to be extremely profitably or become bottomless pits with no hope of survival due to the impact caused by anyone of the above cited reasons.

6. Entrepreneur:

ADVERTISEMENTS:

A business comes into being because of an individual who dreams big. He takes the initiative, invests funds, and sets the ball rolling. The person who recognizes the need for a product or service and bears the entire risk is known as an entrepreneur. He visualizes a business, combines the various factors of production, and puts them into a going concern. He is the key figure who plans everything and gets the business on rails. It is impossible to think of a business without an enterprising entrepreneur.

7. Creation of Value:

Any business creates and delivers value to the consumers. Creation of utility is the main feature of the business. When raw materials are converted into finished goods, it creates form utility. The goods are transported from the place of production to the ultimate consumer, which creates a place of utility. The process of storing goods when they are not required and then supplying them at a time when they are needed is called creation of time utility. At every stage, businesses deliver value to the consumers.

Businesses survive and flourish as long as they are able to meet the expectations of their customers. While doing so, they should run ahead of the competition and deliver service at affordable prices (remember McDonald’s) whenever and wherever the customers want them in an innovative manner (remember McVeggie, Big Spicy Paneer Wrap, McSpicy Paneer, McAloo Tikki, Potato Wedges, Veg McMuffin, etc., mostly vegetarian items for Indian customers).

8. Defining a Business:

A business, thus, is an economic activity initiated by an entrepreneur. It involves regular production and exchange of goods and services. The purpose is to make money by offering what the customers want. The whole show is run in an environment full of risks and uncertainties of various kinds. Exhibiting moral, ethical, and legally acceptable behaviour is essential if the businessman wants to be a long distance runner. Above all, business requires funds, and placement of these funds to the best advantage.

What is Business – Scope

Business activities carried on by different organisations can be summarised as follows:

ADVERTISEMENTS:

(1) Processing and Manufacturing Activities – These include manufacturing, processing, assembling to make the final products either from raw materials or by using different semi-finished or intermediate products. Making televisions, refrigerators, scooters, cars, furnitures, shoes, dress materials etc., are some of the manufacturing activities.

(2) Service Activities – The facilitating or auxiliary activities contributing to the flow of goods and services to the consumers like transportation, warehousing, insurance, advertising, banking, financing, hotels, etc., are some of the examples of service activities.

(3) Mining/ Extraction Activities – Activities related to mining of minerals and metals like iron ore, coal, copper, aluminium, etc. Activities related to exploration of petroleum products, natural gas, etc.

(4) Trading Activities – Activities carried on by the traders like wholesaler, retailer, factor, commission agent and broker engaged in distribution of goods and services are trading activities.

(5) Agricultural Activities – Growing of various crops like wheat, rice, sugarcane, vegetables, fruits, etc. Agricultural activities also include food processing industries engaged in preparing fruit juice, jam, sauce, etc.

What is Business – 7 Characteristics: An Economic Activity, Production or Procurement of Goods and Services, Sale or Exchange of Goods and Services and a Few Others

The main characteristics of business are as follows:

ADVERTISEMENTS:

1. An Economic Activity:

Business is an economic activity as it is undertaken with the aim of earning money or livelihood and not because of love, affection or any other psychological reason.

2. Production or Procurement of Goods and Services:

Business exists to satisfy wants of the consumers. So, every business either itself produces the goods or services or procures them from others in order to sell them to consumers or users. Goods may consist of consumer goods (like sugar, pen, etc.) or capital goods (like machinery, furniture, etc.). Services may include facilities in the form of transportation, banking, electricity, etc.

3. Sale or Exchange of Goods and Services:

ADVERTISEMENTS:

All business activities are directly or indirectly concerned with transfer or exchange of goods and services for value. Production or purchase of goods for personal consumption cannot be called a business activity as there is no sale or transfer for value. For example, cooking food at home for the family is not business. However, cooking food in a restaurant for customers and charging from them is business.

4. Dealings in Goods and Services on a Regular Basis:

Business involve exchange of goods and services on a regular and recurring basis. A single transaction of sale or purchase does not constitute business. For example, if a person sells his mobile at a profit, it does not constitute business. However, if he keeps a stock of mobile sets and regularly sells them (either from shop or from home), then it will constitute business.

5. Profit Earning:

The main aim of every business is to earn profit. No business can survive for long without earning profit. For example, business selling goods at less than cost or free of cost (as charity), cannot continue for long. Due to this reason, businessmen make all possible efforts to maximise profits.

If a businessman continuously suffers loss in a particular business activity, then he will have to leave it sooner or later.

ADVERTISEMENTS:

6. Uncertainty of Return:

Every business aims to earn profits. However, there exists uncertainty of return that the businessman may earn on his investment. It is not certain as to what amount of profit will be earned. There is always a possibility of losses, inspite of best efforts put into the business.

7. Element of Risk:

Risk is the uncertainty associated with an exposure to loss. It is related with certain factors like changes in consumer tastes and fashions, changes in methods of production, strike, increased competition, fire, theft, etc. Every business in the world involves some degree of risk. No business can altogether do away with risk.

What is Business – 8 Major Objectives: Market Positioning, Innovation, Productivity, Profitability, Motivating Workers for Improved Performance and a Few Others

Objectives are the goal of effort—an end toward which effort is directed and on which resources are focused, usually to achieve an organisation’s strategy. According to Peter F. Drucker, “To manage a business is to balance a variety of needs and goals. And this requires multiple objectives.” Thus business managers should set separate objectives in every ‘core (strategic) area’ which has direct bearing on a firm’s long-term survival and growth. Peter F. Drucker has identified eight such key areas. And in his view one separate objective has to be set in each area.

The objectives are of the following:

ADVERTISEMENTS:

Objective # 1. Market Positioning:

It refers to a marketing strategy which will position a company’s products and service against those of its competitor’s, e.g., the position of ‘Dettol’ against that of ‘Savlon’. A progressive organisation must aim at increasing its market positioning by offering quality products at competitive prices and attracting customers on a permanent basis by developing brand loyalty products.

At international level, Apple computers enjoys No.1 position in the market and is always trying to introduce new models to retain its position and even improve its market share. A positioning strategy seeks to differentiate the firm’s brand from those of its competitors in terms of product characteristics and ‘image’ so as to maximise sales potential.

Objective # 2. Innovation:

Management has only two functions to perform, viz., innovation and marketing. Innovation is the process through which new products, concepts, services, methods, or techniques are developed. It is essentially commercial application of a new idea. Product innovation involves a new or modified product. Process innovation involves a new or modified way of making a product.

Technological innovation leads to disappearance of an old product or production process and emergence of a new product or a new method of producing an old product. The major aspects of innovations are the speed and scale of their adoption in the market place. Innovations are absolutely essential for a business enterprise to survive in today’s fiercely competitive environment. For example, Samsung introduced new technology in air conditioners, having extra cooling power.

Objective # 3. Productivity:

Productivity is the ratio of output to inputs used in the production process. It is a test of efficiency of an enterprise. Productivity can be raised by ensuring more effective utilisation of existing resources. If this happens, cost of production per unit falls.

Objective # 4. Profitability:

Profit maximisation is not the only objective of a business firm. However, if it does not earn satisfactory profit it cannot reward the owners (shareholders) adequately. And it cannot discharge its obligations to other stockholders as also the whole society.

Objective # 5. Motivating Workers for Improved Performance:

A business firm should be concerned with its main resources—the human factor. By motivating the workers and through morale building, it is possible to improve workers’ efficiency. This, in its turn, will lead an increase in overall productivity.

Objective # 6. Physical and Financial Resources:

A business enterprise requires various resources or factor inputs (both physical and financial) for producing different types of goods and services needed by its customers such as plant equipment, machinery, building, materials, as also money. Money serves as working capital. It is also needed to meet other expenses associated with the production and distribution of goods and services. A business seeks to procure various resources at low cost through bulk purchase and use them efficiently. In other words, a firm seeks to achieve economy in resource acquisition and efficiency in resource use, so as to keep costs down and profits high.

Objective # 7. Managerial Performance:

Business managers perform the various functions of a business, such as planning, organising, directing, controlling and coordinating. They also set targets in various functional areas such as production, marketing, finance and personnel. In addition, a firm can thrive in the long run by trying to make continuous improvement in its operation through management development. This is to be achieved by undertaking various types of programmes.

Objective # 8. Social Responsibility:

A business is a part of society. So it must discharge its responsibility to the society, by such measures as protection of the physical environment, community development and generation of gainful employment opportunities.

A primary challenge for organisations of the 21st century will be to recognise and respond to the needs of their stakeholders. Stakeholders are all the people who stand or gain or lose by the policies and activities of a business such as customers, employees, shareholders, suppliers, dealers (retailers), banks, people in the community, the media, environmentalists and leaders of the ruling party. So, the need for the business to make profits may be balanced against the needs of employees to earn sufficient income or the need to protect the environment.

What is Business – Classification: Based On Size, Ownership, Processes Used and Products/Services

These may be classified on the basis of:

1. Size,

2. Ownership,

3. Processes used, and

4. Products/services.

1. Based on Size:

Based on size, businesses may be classified as large scale and small and medium enterprises. Large-scale units carry out operations world-wide. They use sophisticated technology, diversify into various fields, deploy professional managers, and compete globally in order to establish their brand and earn profits. Small and medium enterprises are bound by certain investment norms established under the Micro, Small & Medium Enterprises Development (MSMED) Act, 2006.

According to this Act, small, medium and micro enterprises are defined thus:

Manufacturing Sector:

i. Micro enterprise – An undertaking wherein the investment in plant and machinery does not exceed Rs. 25 lakh.

ii. Small enterprise – An undertaking wherein the investment in plant and machinery does not exceed Rs. 5 crore.

iii. Medium enterprise – An undertaking where the investment in plant and machinery is above Rs. 5 crore but below Rs. 10 crore.

Service Sector:

i. Micro enterprise – An undertaking where the investment in equipment does not exceed Rs. 10 lakh.

ii. Small enterprise – An undertaking where the investment in equipment is above lakh but below Rs. 2 crore.

iii. Medium enterprise – An undertaking where the investment in equipment varies between Rs. 2 crore and Rs. 5 crore.

i. Micro enterprise – An undertaking wherein the investment in plant and machinery does not exceed Rs. 25 lakh.

ii. Small enterprise – An undertaking wherein the investment in plant and machinery does not exceed Rs. 5 crore.

iii. Medium enterprise – An undertaking where the investment in plant and machinery is above crore but below Rs. 10 crore Service sector.

iv. Micro enterprise – An undertaking where the investment in equipment does not exceed Rs. 10 lakh.

v. Small enterprise – An undertaking where the investment in equipment is above Rs. 10 lakh but below Rs. 2 crore.

vi. Medium enterprise – An undertaking where the investment in equipment varies between Rs. 2 crore and Rs. 5 crore.

Ancillary Industrial Undertakings – An undertaking that sells not less than 50 per cent of its production to other undertakings and wherein investment in plant and machinery does not exceed Rs. 10 crore (revised from the earlier Rs. 5 crore limit).

Tiny Enterprises – An undertaking where the investment in plant and machinery does not exceed Rs. 25 lakh.

2. Based on Ownership:

On the basis of ownership, businesses can be classified as public sector and private sector. Public sector units (such as – SAIL, NTPC, ONGC, IOC) are owned by the government and are aimed at employment generation, distribution of wealth to all sections of society, offering better quality goods at affordable prices.

In India, many of these governments enterprises were started in the early 1970s and 1980s. A private enterprise (such as – Tata Steel, Reliance Industries, Spencers, Big Bazar) is run by entrepreneurs. They compete with local as well as global firms while trying to deliver value to customers. Where the enterprise is owned by the government, as well as private entrepreneurs, it is called a joint enterprise.

3. Based on Processes Used:

Based on processes used, businesses may be classified thus:

i. Extractive businesses are concerned with supplying commodities, which are extracted from the earth (for example, farming, mining, lumbering, hunting, and fishing). The products of these industries—such as – oils, minerals—are generally used by manufacturing and constructive industries for making finished goods.

ii. Genetic-businesses refer to industries under which plants and animals are grown for the purpose of sale to the consumers (for example, breeding plants in nurseries, cattle rearing, horticulture, farming, and sericulture).

iii. Construction businesses are concerned with the construction of buildings, bridges, dams, canals, and roads. The raw materials that are used by these industries are the products of manufacturing industries.

iv. Business provides not only goods but also services. Services industries do not produce any tangible goods. These are engaged in providing services to the public.

v. Manufacturing businesses are those, which convert raw materials or semi-finished goods into finished products. Articles of daily use are mostly produced by manufacturing units.

Manufacturing industries may further be classified thus:

a. Analytical – Here a basic raw material is analysed and separated into a number of products. For example, an oil refinery separates crude into petrol, diesel, kerosene, gasoline, and lubricating oil.

b. Synthetic – In this case two or more products are synthesized or combined to manufacture a new product. Fertilizers, Cosmetics, Paints, Plastics, Medicines are manufactured by synthetic industries

c. Processing – Here, the raw material is processed through different stages of production. In the paper industry, for example, bamboo is converted into pulp, and after cleansing, converted into different types of paper (likewise in sugar, steel and textile industries.)

d. Assembling – Here, the various parts or components are brought together to produce a finished product. Televisions, radios, automobiles, and air conditioners are examples of assembly industry.

4. Based on Products/Services Offered to Consumers:

Based on type of products manufactured, we can classify businesses into three categories – (i) consumer products business, (ii) industrial products business, and (iii) services business. Firms that sell their products (such as – air conditioners, radio, television, soap, toothpaste and clothing) to final consumers are said to be in the consumer products business. Firms that manufacture goods that are used for the production of other goods such as – machines, tools, and equipment are said to be in the industrial products business.

Businesses that offer services to customers, such as – information technology, call centres, back office operations, media, and entertainment, Web development operations, medical transcription, communication, and networking services, are said to be in the services business. A variety of service providers in the field of banking, insurance, transportation, and hotels may be included in this category.

There could be various other ways of classifying the types of business. Based on geographical reach and location, one can classify businesses into two types – domestic companies and multinational companies. Domestic units carry out business within, the boundaries of a country.

Multinational companies carry out operations on a global scale. One can also classify businesses into trading, assembling and manufacturing units. On the basis of distribution, businesses can be put into two categories – wholesale and retail business. There could be online businesses (such as – Flipkart, Bookadda) and offline businesses (such as – a web designer).

In addition to the above, business activities may also be classified into three broad categories, namely:

i. Industry,

ii. Commerce, and

iii. Trade.

i. Industry:

Industry may be broadly classified into primary, secondary, and tertiary industries. Primary industries extract materials from natural resources; secondary industries use the products of primary industries, and convert them into outputs through manufacturing or construction operations; and tertiary industries offer services to both primary and secondary industries—namely, transportation, banking, warehousing, etc. Primary industries may be either extractive or genetic, and secondary industries may be either manufacturing or construction.

ii. Commerce:

The term ‘commerce’ refers to all those activities that facilitate the transfer of goods and services from producers to consumers. It is an important link that helps producers get connected to end users. Facilitating services like transportation, warehousing, insurance, banking, advertising, packing help the smooth, and easy transfer of goods from producers to consumers.

iii. Trade:

Trade implies sale, transfer or exchange of goods and services. The basic objective of trade is to make the goods and services available to those who need them and are willing to pay for them. There can be businesses doing domestic trade as well as foreign trade. Domestic trading can be in the form of wholesale or retail business. Trade between nations is called international business.

International business might involve imports (purchasing goods from a foreign country), as well as exports (selling domestic goods in a foreign country). To facilitate trade within and outside the country, we have service providers operating within a country. These are popularly known as aids to trade or auxiliaries to trade—such as transportation, warehousing, insurance, banking, and advertising.

What is Business – 3 Important Diversification: Acquiring and Restructuring, Transferring Competencies and Economies of Scope

Most companies first consider diversification when they are generating financial resources, therefore it is excess to maintain competitive advantage in their original or core business. The diversified company can generate value in three main routes.

They are listed below:

1. Acquiring and restructuring

2. Transferring competencies

3. Economies of scope

1. Acquiring and Restructuring:

Acquiring and restructuring involved by acquiring and restructuring of poorly- run enterprises. A restructuring strategy rests on the presumption that an efficiently-managed company can create value by acquiring inefficient and poorly-managed enterprises and improving their efficiency, this approach can be considered diversified because the acquired company does not have to be in the same industry as the acquiring company for the strategy to work. Improvements in the efficiency of an acquired company can come from a number of sources.

They are listed below:

i. The acquiring company usually replaces the top management team of the acquired company with more aggressive top management team.

ii. The new top management team is encouraged to sell – off any unproductive assets like executive’s jets and elaborate corporate head-quarters and to reduce staffing levels.

iii. The new top management team is also encouraged to intervene in the running of the acquired business to seek out routs of improving the units’ efficiency, quality, innovativeness, and customer responsiveness.

iv. To motivate the new top management team and other employees of the acquired unit to undertake such actions, increases in their pay may be linked to industries in the performance of the acquired unit.

v. The acquiring company often establishes performance goals for the acquired company.

2. Transferring Competencies:

Companies diversification strategy on transferring competencies seek out new business, related to their existing business by one or more value creation functions, for instance, manufacturing. Marketing, materials management and R&D. they want to create value by drawing on the distinctive skills in one or more of their existing value creation function in order to improve the competitive position of the new business. It can improve the efficiency of their existing business.

It arises when two or more business units share resources like:

i. Manufacturing facilities

ii. Distribution channels

iii. Advertising

iv. R&D Costs

Each business unit utilized better and reduced to operating cost.

What is Business – 4 Major Factors: Impact of Economic Growth on Business Performance, Impact of Inflation and Government Influence on Economic Conditions

Factor # 1. Impact of Economic Growth on Business Performance:

Economic growth represents the change in the general level of economic activity. Sometimes economic growth is strong, and other times it is relatively weak.

When U.S. economic growth is stronger than normal, the total income level of all U.S. workers is relatively high, so there is a higher volume of spending on products and services. Since the demand for products and services is high, firms that sell products and services should generate higher revenue.

Whereas strong economic growth enhances a firm’s revenue, slow economic growth results in low demand for products and services, which can reduce a firm’s revenue. Even firms that provide basic products or services are adversely affected by a weak economy because customers tend to reduce their demand. For example, the demand for coffee at Starbucks is affected by general economic conditions.

Since specialty coffee is not really a necessity, demand for it is stronger when consumers are earning a relatively high income and can afford it. The demand for soft drinks and bottled water is also affected, as some people rely more on tap water under weak economic conditions.

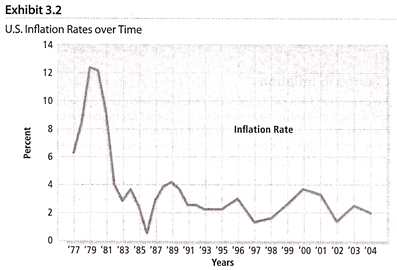

Factor # 2. Impact of Inflation:

Inflation is the increase in the general level of prices of products and services over a specified period of time. The inflation rate can be estimated by measuring the percentage change in the consumer price index, which indicates the prices on a wide variety of consumer products such as grocery products, housing, gasoline, medical services, and electricity.

The annual U.S. inflation rate is shown in Exhibit 3.2. The inflation rate was generally higher in the 1970s than it has been in more recent years, which was partially attributed to an abrupt increase in oil prices then.

Inflation can affect a firm’s operating expenses from producing products by increasing the cost of supplies and materials. Wages can also be affected by inflation. A higher level of inflation will cause a larger increase in a firm’s operating expenses. A firm’s revenue may also be high during periods of high inflation because many firms charge higher prices to compensate for their higher expenses.

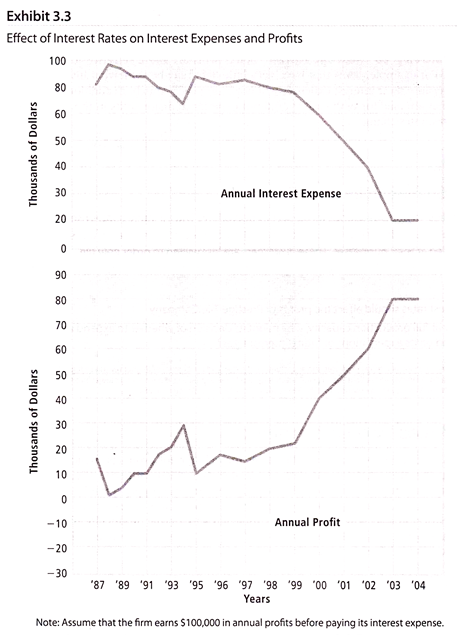

Factor # 3. Impact of Interest Rates:

Interest rates determine the cost of borrowing money. They can affect a firm’s performance by having an impact on its expenses or on its revenue.

Firms closely monitor interest rates because they determine the amount of expense a business will incur if it borrows money. If a business borrows $100,000 for one year at an interest rate of 8 percent, the interest expense is $8,000 (computed as .08 X $100,000). At an interest rate of 15 percent, however, the interest expense would be $15,000 (computed as .15 X $100,000).

Imagine how the interest rate level can affect some large firms that have borrowed more than $1 billion. An interest rate increase of just 1 percent on $1 billion of borrowed funds results in an extra annual interest expense of $10 million.

Changes in market interest rates can influence a firm’s interest expense because the loan rates that commercial banks and other creditors charge on loans to firms are based on market interest rates.

Even when a firm obtains a loan from a commercial bank over several years, the loan rate is typically adjusted periodically (every six months or year) based on the prevailing market interest rate at that time.

Exhibit 3.3 illustrates the annual interest expense for a reputable U.S. firm that borrows $1 million from a bank each year and earns $100,000 in annual profits before paying its interest expense. The interest expenses are adjusted each year according to the market interest rates prevailing in the United States during that year.

As this exhibit shows, interest rates can significantly influence a firm’s profit. Firms incurred much higher interest expenses in the early 1980s because interest rates were so high then.

Since interest rates affect the cost of financing, some possible projects considered by the firm that would be feasible during periods of low interest rates may not be feasible during periods of high interest rates. That is, the project may not generate an adequate return to cover financing costs. Consequently, firms tend to reduce their degree of expansion when interest rates are high.

Factor # 4. Government Influence on Economic Conditions:

The federal government can influence the performance of businesses by imposing regulations, such as the environmental regulations or by enacting policies that affect economic conditions.

Monetary Policy:

In the United States, the term money supply normally refers to demand deposits (checking accounts), currency held by the public, and traveler’s checks. This is a narrow definition, as there are broader measures of the money supply that count other types of deposits as well. Regardless of the precise definition, any measure of money represents funds that financial institutions can lend to borrowers.

The U.S. money supply is controlled by the Federal Reserve System (“the Fed”), which is the central bank of the United States. The Fed sets the monetary policy, which represents decisions on the money supply level in the United States. The Fed can easily adjust the U.S. money supply by billions of dollars in a single day.

Because the Fed’s monetary policy affects the money supply level, it affects interest rates. When the Fed affects interest rates with its monetary policy, it directly affects a firm’s interest expenses. Second, it can affect the demand for the firm’s products if those products are commonly purchased with borrowed funds.

Fiscal policy involves decisions on how the federal government should set tax rates and spend money. These decisions are relevant to businesses because they affect economic growth and therefore can affect the demand for a firm’s products or services.

What is Business – 4 Market Conditions for Creating a New Business: Demand, Competition, Labor Conditions and Regulatory Conditions

Before creating a new business for a particular market, the following conditions in that market should be considered:

(i) Demand

(ii) Competition

(iii) Labour conditions

(iv) Regulatory conditions

(i) Demand:

Every product has its own market, where there are consumers who purchase the product and businesses that sell the product. In the market for personal computers (PCs), there is demand by millions of people for PCs, and there are many businesses (such as Dell and Hewlett-Packard) that produce PCs to accommodate that demand. There is also a market for services such as those provided by hairstylists, dentists, and mechanics.

Since these services cannot be shipped, the demand for services within an area is accommodated by firms within that area. For example, the entire demand for auto mechanic services in a specific small town may be accommodated by a total of three auto mechanic businesses. Thus, there are many markets for a single service, with each market representing a specific area.

Over a given time period, firms in a specific market can perform much better than others because the total demand for the products in that market is high. The demand for most products is partially influenced by general economic conditions because consumers tend to buy more products and services when the economy is strong and they have a good income.

The demand is also influenced by conditions within the specific market of concern. The demand for baby clothes is highly dependent on the number of children that are born. The demand for hotels in Florida during the winter is partially dependent on the weather in the northern states. In cold winters, more tourists travel to Florida.

The demand within a particular market changes over time. When it increases, the businesses within that market tend to benefit because their sales increase. Entrepreneurs tend to develop new businesses in markets where there is a strong demand so that they can benefit from that demand.

Just as an increase in demand is beneficial to firms in that market, a decline in demand has adverse effects. Consider the case of Bell Sports Corporation, which was once the largest producer of motorcycle helmets. It experienced a decline in business because the demand for these helmets leveled off.

As the demand for bicycles increased, Bell switched its production process to make bicycle helmets instead. It also began to produce other bicycle accessories, such as child seats, safety lights, and car racks. In this way, it diversified its product line so that it was not completely reliant on its bicycle helmet business.

(ii) Competition:

Each business has a market share, which represents its sales volume as a percentage of the total sales in a specific market. If the total sales in the market for a particular product are $ 10 million this year, a firm that experienced sales of $2 million has a market share of 20 percent (computed as $2 million divided by $10 million). That is, the firm has 20 percent of the market.

If the competition within a particular market is limited, firms can more easily increase their market share and therefore increase their revenue. In addition, they may also be able to increase their price without losing their customers. Therefore, entrepreneurs prefer to pursue markets where competition is limited.

When competition in a particular market increases, it can reduce each firm’s market share, thereby reducing the quantity of units sold by each firm in the market. Second, a high degree of competition may force each firm in the market to lower its price to prevent competitors from taking away its business. Consider the intense competition recently in the market for long-distance phone services.

Firms that compete within a market for a particular product or service typically want to increase their market share. However, all firms cannot increase their share simultaneously. One firm’s increase in market share occurs at the expense of another firm’s decline in market share. For example, suppose that in a particular market (such as a small town), there will be a total of 6,000 visits to dentists this year.

That is, the total demand for dentistry services in one year is 6,000. At this time, there are two dentists in the market. If a new dentistry business enters the market, any customers that it attracts will represent a reduction in business for the other two dentists. As a new business penetrates (enters) a market, it takes a portion of the market from other firms.

Thus, it gains market share, while other firms may lose market share. Since its competitors prefer not to give up any of their market share, they may use various business strategies to counter the entrance of a new business into the market. It is difficult for a new business to continually increase its market share, especially when additional new businesses enter the market.

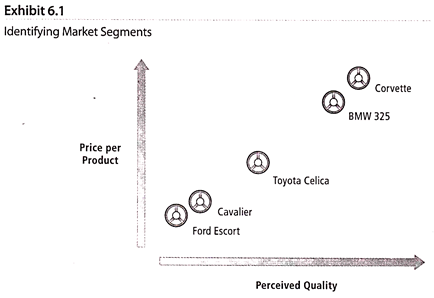

Competition within Segments:

Each market has segments, or subsets that reflect a specific type of business and the perceived quality. Thus, a market can be narrowly defined by type of business and quality. Segmenting the market in this way allows a firm to identify its main competitors so that they can be assessed.

A market can be segmented by specific types of customers. For example, in the car rental market, some firms (such as Hertz) focus heavily on business customers, while others (such as Dollar and Payless) focus more on individuals who are on vacation. Thus, an entrepreneur who plans to create a new car rental business must decide which segment to enter. This decision will affect the types of customers that it targets for its business.

A market may also be segmented by quality. Exhibit 6.1 shows different quality segments (based on customer perceptions) in the market for small cars. Each type of car in this market is represented by a point. Some cars, such as the BMW and the Corvette, are perceived to have high quality (measured according to engine size and other features that customers desire) and a relatively high price.

Other cars have a moderate quality level and a lower price, such as the Toyota Celica. The Ford Escort and the Chevy Cavalier represent cars in a lower quality and price segment. Because each consumer focuses only on one particular market segment, the key competitors are within that same segment.

For example, the Escort and Cavalier are competitors within the low-priced segment. The Escort is not viewed as a competitor to the higher-priced cars. If a car company wants to produce a new small car, it assesses the competition according to the segment that it plans to target.

(iii) Labor Conditions:

Some markets have specific labor characteristics. The cost of labor is much higher in industries such as health care that require specialized skills. Unions may also affect the cost of labor. Some manufacturing industries, particularly those in the northern states, have labor unions, and labor costs in these industries are relatively high.

Industries that have labor unions may also experience labor strikes. Understanding the labor environment within an industry can help an entrepreneur estimate labor expenses and decide whether a new business could produce products at lower costs than existing firms.

(iv) Regulatory Conditions:

The federal government may enforce environmental rules or may prevent a firm from operating in particular locations or from engaging in particular types of business. For example, Blockbuster is affected by state and federal regulations regarding advertising, consumer protection, provision of credit, franchising, zoning, land use, health and safety, and working conditions.

Although all industries are subject to some form of government regulation, some industries face especially restrictive regulations. Automobile and oil firms have been subject to increased environmental regulations.

Firms in the banking, insurance, and utility industries have been subject to regulations on the types of services they can provide. Companies such as Amazon.com that rely heavily on the Internet for their business are exposed to some additional regulations governing the Internet and e-commerce.

For example, they could be affected by laws regarding the protection of consumer data. If more regulations are implemented to ensure greater protection, the costs to Amazon.com of running its business could increase. Entrepreneurs who wish to enter any industry must recognize all the regulations that are imposed on that industry.

Firms that are already operating in an industry must also monitor industry regulations because they may change over time. For example, recent reductions of regulations in the banking industry have allowed banks more freedom to engage in other types of business. Some banks have attempted to capitalize on the change in regulations by offering new services.

What is Business – Role of Profit: Incentive, Expansion, Indication of Efficiency and Reputation

About the role of profit, the famous US writer, Richard Bach, has opined as follows:

I don’t want to do business with those who don’t make profit because they can’t give the best service.

Thus, the role of profit in business is as follows:

1. Incentive:

Profit is a strong incentive for an entrepreneur to start and run a business. An incentive is an object which motivates a person to do work in a better way. Stronger the incentive, higher is the motivation for doing work in a better way.

2. Expansion:

Profit is necessary for the expansion of business in the long run as a part of profit is invested in the business to expand it. Expansion of business is necessary for achieving its objectives.

3. Indication of Efficiency:

Profit is an indication of efficiency of a business. Thus, more profit means higher efficiency. However, this profit should not come through unethical practices but only through fair means.

4. Reputation:

Reputation is attached to a business that earns higher profit by fair means. This reputation itself becomes the source of motivation to the entrepreneur to do better and better in his business.

Is Profit the Sole Objective of Business?

The answer to the above question is important because in common parlance it is said, ‘business is meant for earning profit’. Even when a businessman asks another businessman about how the business is running, he generally means how much profit the business is earning.

In the light of the above comments, it can be said that profit is not the sole objective of business but it has many objectives—economic objectives and social objectives. Profit objective is only one part of the economic objective. Since a businessman achieves various other objectives during the process of performing business activities, these remain silent in common parlance. This is the reason people do not appreciate a businessman who earns huge profits by unethical means.