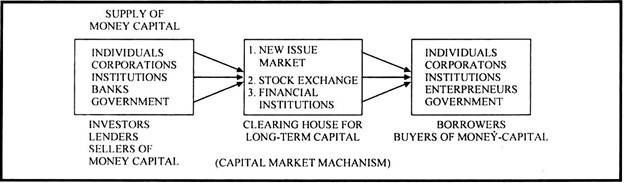

This article throws light upon the three main components of capital market. The components are: 1. New Issue Market 2. Secondary Market 3. Financial Institutions.

Capital Market: Component # 1. New Issue Market:

The new issue market represents the primary market where new securities, i.e., shares or bonds that have never been previously issued, are offered. Both the new companies and the existing ones can raise capital on the new issue market.

The prime function of the new issue market is to facilitate the transfer of funds from the willing investors to the entrepreneurs setting up new corporate enterprises or going in for expansion. Diversification, growth or modernisation. Besides, helping corporate enterprises in securing their funds, the new issue market canalizes the savings of individuals and others into investments.

ADVERTISEMENTS:

The two facets of this market, i.e. supply and demand, are represented by the issuing companies and the investors respectively. But then the organisation of the new issue market is not complete without the specialised agencies, intermediaries and institutions, etc., which promote issues of new securities and help in selling, transferring, underwriting etc.

These agencies include financial institutions, underwriters, brokers, merchant bankers, etc.

As the new issue market directs the flow of savings into long-term investments, it is of paramount importance for the economic growth and industrial development of a country. The availability of financial resources for corporate enterprises, to a great extent, depends upon the status of the new issue market of the country.

It must also be noted that although the functions and organisation of the new issue market are quite different from that of the secondary (stock) market, the sentiment in the stock market influences the activity in the new issue market.

ADVERTISEMENTS:

The stock market is more sensitive and reacts fast to the changes in the economic, political and business conditions of a country. But then this affects the new issue market also. The historical study of the activity in the two markets show that whenever there has been boom in the stock market, there has been increased activity in the new issue market also.

Capital Market Instruments:

Primary market is a market for raising long-term finance by the issue of new corporate securities.

The corporate securities that are dealt in primary market can be classified under two categories:

ADVERTISEMENTS:

1. Ownership Securities or Capital Stock, and

2. Creditorship Securities or Debt Capital.

ADVERTISEMENTS:

Capital Market: Component # 2. Secondary Market:

The secondary market is a market where existing securities are purchased and sold. Stock market represents the secondary market where existing securities (shares and debentures) are traded; Stock exchange provides an organised mechanism for purchase and sale of existing securities. By now, we have 23 stock approved stock exchanges in our country.

The investors want liquidity for their investments. The securities which they hold should easily be sold when they need cash. Similarly there are others who want to invest in new securities. There should be a place where the securities may be purchased and sold.

Stock exchanges provide such a place where securities of different companies can be purchased and sold. Stock exchange is a body of persons, whether incorporated or not, formed with a view to helping, regulating and controlling the business of buying and selling of securities.

ADVERTISEMENTS:

Stock exchanges are organised and regulated markets for various securities issued by corporate sector and other institutions. The stock exchanges enable free purchase and sale of securities as commodity exchange allow trading in commodities. The following definitions explain the meaning and scope of stock exchanges.

Definitions of Stock Exchange:

Pyle. “Security exchanges are market places where securities that have been listed thereon may be bought and sold for either investment or speculation.”

Stock exchanges allow trading in securities both to the genuine investors and speculators.

ADVERTISEMENTS:

Securities Contract (Regulation) Act, 1956. “Stock exchange means anybody of individuals, whether incorporated or not, constituted for the purpose of assisting, regulating or controlling the business of buying, selling in securities.”

According to this definition, the stock exchange allows trading in securities under certain rules and regulations.

Hartely Withers “A Stock Exchange is something like a vast warehouse where securities are taken away from the shelves and sold across the countries at a fixed price in a catalogue which is called the official list.”

Hartley calls stock exchange a warehouse where all securities are kept and traded on specified prices. It may not always be that every type of security is purchased for sale; there may be investors who do not bring their securities to the market but keep them only as investments.

ADVERTISEMENTS:

Husband and Dockeray “Securities or stock exchanges are privately organised markets which are used to facilitate trading in securities.” As per this definition the stock exchanges are the organised places where securities are purchases and sold.

Characteristics of Stock Exchanges:

From the definitions given earlier, the following characteristics or salient features of stock exchange come out:

i. It is a place where securities are purchased and sold.

ii. A stock exchange is an association of persons whether incorporated or not.

iii. The trading in a stock exchange is strictly regulated and rules and regulations prescribed for various transactions.

ADVERTISEMENTS:

iv. Both genuine investors and speculators buy and sell shares.

v. The securities of corporations, trusts, governments, municipal corporations etc. are allowed to be dealt at stock exchanges.

Listing of Securities:

Listing of securities means permission to quote shares and debentures officially on the trading floor of the stock exchange. Every security issued by companies cannot be traded at a stock exchange. The stock exchanges fix certain standards which the company must fulfill before getting the securities listed.

Objectives of Listing:

The main objectives of listing of securities are:

ADVERTISEMENTS:

i. To ensure proper supervision and control of dealings in securities.

ii. To protect the interests of shareholders and the investors.

iii. To avoid concentration of economic power.

iv. To assure marketing facilities for the securities.

v. To ensure liquidity of securities.

vi. To regulate dealings in securities.

ADVERTISEMENTS:

vii. To require promoters to have a reasonable stake in the company.

Advantages of Listing:

Following are some of the advantages of listing securities:

i. Publicity of Securities:

The listed securities get wide publicity in papers etc. The rates of securities are regularly quoted for the benefit of investors. The names of companies are also mentioned along with the rates and the investors become familiar with the securities.

ii. Protection of Investors’ Interest:

ADVERTISEMENTS:

The securities are traded according to certain rules and regulations. The listed companies have to provide full information about assets, liabilities etc. to the stock exchange. The investors’ interests can be protected disclosing full information about the companies. They can make their own decisions by analysing financial statements of those companies whose securities they want to purchase.

iii. Ensures Liquidity:

The listed securities have a ready market at stock exchange. A large number of buyers and sellers are always present at exchanges to trade in securities. The prices offered for securities are also competitive.

iv. Better Goodwill:

The securities listed in exchanges have better goodwill in the market. The securities are rated high in the market and banks accept such securities as collateral securities.

Screen Based Trading:

ADVERTISEMENTS:

Screen Based Trading has been a major development in the secondary market in India. It has transformed the character of the entire Indian stock market. Under this system of trading, the computer screen replaces the trading ring and distant participants can trade with each other through computer network.

A large number of participants distributed widely over the country, can trade simultaneously at high speeds. This system permits the market participants to have a full view of the market which increases their confidence and helps to establish greater transparency.

NSE and OTCEI have set up these computerized exchanges. Some of the benefits of screen based trading include:

i. By using very small terminals of NSE the members can trade with each other with much more ease and comfort sitting at their door steps.

ii. It provides full information to the investors about the market.

iii. It enables members all over the country to trade with each other simultaneously.

iv. It has avoided the need of the people to assemble on the floor of the stock exchange for trading.

v. It ensures greater transparency and has increased the confidence of the people.

Functionaries of Stock Exchanges:

Functionaries of stock exchanges refer to those persons or individuals or institutions who perform the functions of a Stock Exchange and who are the registered members of the exchange.

The following are the various types of functionaries who function at the stock exchange:

i. Jobbers:

Jobbers are security merchants dealing in shares, and debentures as independent operators. They buy and sell securities on their own behalf and try to earn through price changes. Jobbers cannot deal on behalf of public and are barred from taking commission.

They directly deal with brokers who in turn make transactions on behalf of public. Jobbers generally quote two prices one at which he is prepared to purchase and the other at which he is prepared to sell a particular security.

The difference between the two prices is the Jobber’s profit which is technically known as Jobber’s turn. For example a jobber may quote the equity shares of Bindal Agro at Rs. 95-Rs. 96. This implies that a Jobber is prepared to purchase these shares at Rs. 95 each and sell at Rs. 96 each. The difference between these two prices is Jobber’s profit or the Jobber’s turn.

The London Stock Exchange has two types of members known as Jobbers and brokers. Every members has to declare in the beginning every year whether they will be acting as Jobbers or Brokers. Once he makes a declaration then he has to stick to it.

ii. Brokers:

Brokers are commission agents, who act as intermediaries between buyers and sellers of securities. They do not purchase or sell securities on their behalf. They bring together buyers and sellers and help them in making a deal. Brokers charge commission from both the parties for their service.

Brokers the experts in estimating trends of prices and can effectively advise their client in reaching a fruitful gain. Brokers get orders from investing public and execute the orders through Jobbers and they are entitled to a prescribed scale of brokerage. The investors who do not know the technicalities of stock exchanges are greatly benefited by the experitie of brokers.

iii. Tarawaniwalas:

The members of Bombay Stock Exchange have unofficially divided themselves into two categories:

(i) Brokers and

(ii) Tarawaniwalas.

The latter act both as Jobbers and brokers. A tarawaniwala makes transactions on his own behalf like a Jobber but he may also act as a broker on behalf of the public. They indulge in malpractices to earn profits. They may sell their own securities to their clients when prices are higher and vice-versa.

The distinction between Jobbers of London Exchange and Tarawaniwalas of Bombay Stock Exchange is that the former are not brokers whereas the latter may act both as brokers and Jobbers. Section 15 of the Securities Contract (Regulation) Act prohibits such practices.

It states that no member of a recognised stock exchange shall, in respect of any securities, enter into any contract as a principal with any person other than a member of a recognised stock exchange, unless he has secured the consent or authority of such person and discloses in the memorandum or agreement of sale or purchase that he is acting as principal.

Types of Speculators:

There are four types of speculators who are active on stock exchanges in India. They are known as Bull, Bear, Stag and Lame Duck. These names have been derived from the animal world to bring out the nature and working of speculators.

i. Bull:

A Bull or Tejiwala is an operator who expects a rise in prices of securitieis in the future. In anticipation of price rise he makes purchases of shares and other securities with the intention to sell at higher prices in future.

He being a speculator has no intention of taking delivery of securities but deals only in differences of prices. Such a speculator is called a bull because of resemblance of his behaviour with the bull. A bull tends to throw his victims up in the air. Similarly, a bull speculator tries to raise the prices of securities by placing big purchase orders.

ii. Bear:

A Bear or Mandiwala speculator expects prices to fall in future and sells securities at present with a view to purchase them at lower prices in future. A bear does not have securities at present but sells them at prices in anticipation that he will supply them by purchasing at lower prices in future.

If the prices move down as per the expectations of the bear he will earn profits out of these transactions. Just as a bear presses its victims down to the ground, the bear speculator tends to force down the prices of different securities. When the bear operator starts selling the securities, the bearish pressure gradually forces down the prices.

A bear does not take delivery of securities but takes the difference if prices fall down. In case prices rise then he will have to pay the difference between the prices at which he purchased the securities and the prevailing price on the date of delivery.

A market is said to be bearish when it is dominated by the bear speculators. On the other hand, there is a strong expectation of fall in prices. Pessimism prevails in a bearish market. In case the prices are not falling as expected by the bears then they may start speculator rumours to pressurise prices downwards. It is known as bear raid.

iii. Stag:

A stag is a cautious speculator in the stock exchange. He applies for shares in new companies and expects to sell them at a premium if he gets an allotment. He selects those companies whose shares are in more demand and are likely to carry a premium. He sells the shares before being called to pay the allotment money.

A Stag does not indulge in purchase and sale of shares in the market like a bull and bear. He relies only on the allotment of securities to him. He applies for large number of shares so that he gets some allotment even if there is heavy over subscription.

iv. Lame Duck:

When a bear finds it difficult to fulfill his commitment, he is called struggling like a lame duck.

A bear speculator contracts to sell securities at a later date. On the appointed time he is not able to get the securities as the holders are not willing to part with them. In such situations he feels cornered. Moreover, the buyer is not willing to carry over the transactions.

Stock Exchanges in India:

Despite the fact that unorganised stock market existed in Calcutta since 1830, the first organised stock exchange was set up at Bombay in 1877 under the name of ‘Native Stock and Share Brokers Association’. The next stock exchange which emerged in the country was ‘Ahmedabad Share and Stock Brokers Association’ which was founded in 1894. The third stock exchange was set up at Calcutta in the year 1908.

Though some more stock exchanges were set up before independence but there was no All India Legislation to regulate their working. Every stock exchange followed its own method of working. To rectify this situation and to regulate the working of stock exchanges in the country, the Securities Contract (Regulation) Act was passed in 1956. There were only nine recognised stock exchanges in the country uptil 1981-82.

At present, there are 23 recognised stock exchanges in the country including, Over the Counter Exchange and National Stock Exchange which have also started functioning in our country.

Securities Contracts (Regulation) Act, 1956:

i. Recognition of Stock Exchanges:

The securities can be traded only at Stock Exchanges recognised by Central Government of India in pursuance of the provisions of Securities Contracts (Regulation) Act.

Before giving recognition the Government must satisfy that:

(a) The rules and bye-laws of the applicant stock exchange ensure fair dealing and protect the interests of genuine investors.

(b) It is willing to comply with any conditions that way be imposed by Central Government from time to time.

(c) It is in the interest of trade and public to grant such recognition to the stock exchange.

ii. Control of Central Government:

Under the Act Central Government has been given wide powers to control the working of stock exchanges, some of the controlling powers are:

(a) Every stock exchange has to submit to the government periodical returns of their affairs.

(b) Government may call upon the exchange or members to furnish such information or explanations regarding the affairs of the exchange or transactions of the members as may be required.

(c) Government can appoint persons to enquire into the affairs of the exchange and submit the report in a specified period.

(d) It can regulate the working hours of the exchange.

(e) In the event of any emergency it can suspend the working of an exchange upto a period of seven days.

iii. Controlling Speculation:

Government can curb speculative activities of an exchange.

Some regulations in this direction are:

(a) Option dealings in securities have been banned.

(b) Kerb trading (trading outside the exchange) has been declared illegal.

(c) Life of blank transfer has been restricted to two months.

SEBI’S Role in a Stock Exchange:

Securities and Exchange Board of India has been set up under the SEBI Act, 1992 to protect the interest of investors in securities and to promote the development of and regulate the securities market and for matters connected there with or incidental thereto.

SEBI’S Power in Relation to Stock Exchange:

The SEBI ordinance has given it the following powers:

(i) It may call periodical return from stock exchanges.

(ii) It has the power to prescribe maintenance of certain documents by the stock exchange.

(iii) SEBI may call upon the exchange or any member to furnish explanation or information relating to the affairs of the stock exchange or any members.

(iv) It has power to approve bye-laws of the stock exchange for regulation and control of the contracts.

(v) It can amend bye-laws of stock exchange.

(vi) In certain areas it can licence the dealers in securities.

(vii) It can compel a public company to list its shares.

Superceding Governing Body of Stock Exchange:

If Central Government is of the opinion that the governing body of any recognised stock exchange should be superceded then it may give a written notice specifying the reasons for such action. After giving opportunity to the governing body it may supercede it and appoint person or persons to exercise and perform all the powers and duties of governing body.

Since beginning, SEBI has been working on various matters for improving the working of stock market so that interests of investors are protected.

These measures include broadbasing the stock market with more exchanges and their possible integration, an improvement in the system of trading and settlement procedures, registration of brokers and their associates, greater transparency in the trading activities of brokers and curbing of inside trading by companies and their managements.

SEBI has supported an over the counter market for the listing of smaller companies. The registration of all mutual funds, existing as well as new, has been made essential. Code of advertisements has already been issued to the mutual funds regarding their honesty and fairness to disclose the risk factors involved in their funds.

SEBI has also declared that traders are to be moved to a settlement on delivery basis. The settlement period on exchanges has been shortened. The management structure of the stock exchanges, which have been subject to criticism in the past on account of its broker dominated nature, is now having 50 percent non-broker members.

Further, Stock exchanges are now required to appoint a non-broker professional as an executive director, who remains accountable to SEBI for implementing stock exchanges. Since December 1993, SEBI has banned ‘badla’ or carry forward system and has introduced a foolproof new badla system.

Thus, we can conclude that SEBI is playing an active role in the promotion and regulation of stock exchanges in India. The carry forward system introduced by SEBI is not as liberal as ‘badla’ used to be.

Capital Market: Component # 3. Financial Institutions:

Special Financial institutions are the most active constituent of the Indian capital market. Such organisations provide medium and long-term loans on easy installments to big business houses Such institutions help in promoting new companies; expansion and development of existing companies and meeting the financial requirement of companies during economic depression.

The need for establishing financial institutions was felt in many countries immediately after the Second World War in order to re-establish their war-shattered economies. In underdeveloped countries, the need for such institutions was much more due to a large number of organisational and financial problems inherent in the process of industrialisation.

After independence, a number of financial institutions have been set up at all India and regional levels for accelerating the growth of industries by providing financial and other assistance.

The following are the main special institutions that are most active constituents of the Indian capital market:

i. The Industrial Finance Corporation of India (I.F.C.I.)

ii. The Industrial Credit and Investment Corporation of India (I.C.I.C.I.)

iii. The Refinance Corporation of India (R.F.C.)

iv. State Financial Development Corporations (S.F.Cs.)

v. National Industrial Development Corporation (N.I.D.C.)

vi. State Industrial Development Corporation (S.I.D.Cs)

vii. National Small Industries Corporation (N.S.I.C )

viii. Industrial Development Bank of India (1.D.B.I.)

ix. Unit Trust of India (U.T.I.)

x. Life Insurance Corporation of India (L.I.C.)

xi. Nationalised Commercial Banks (N.C.Bs)

xii. Merchant Banking Institutions (M.B.Is.)

xiii. National Industrial Reconstruction Corporation of India (N.I.R.C.)

xiv. The Credit Guarantee Corporation of India (C.G.C.)

Commercial Banks and the Capital Market:

Commercial banks are also important constituents of capital market but their operations in India have been mainly limited to the purchase and sale of government securities.

However, in recent years, commercial banks have also been increasingly participating in term lending through subscribing to the shares and debentures of special financial institutions. Many commercial banks have also set up separate merchant banking divisions and their financial subsidiaries to provide a variety of financial services.