Here is a compilation of essays on ‘Control in an Organisation’ for class 11 and 12. Find paragraphs, long and short essays on ‘Control in an Organisation’ especially written for school and college students.

Essay on Control in an Organisation

Essay Contents:

- Essay on the Meaning and Definition of Control

- Essay on the Steps Involved in the Control Process

- Essay on the Techniques of Control

- Essay on the Importance of Controlling

- Essay on the Characteristics of Good Control System

- Essay on the Limitations or Shortcomings of Control System

- Essay on the Relationship between Planning and Controlling

Essay # 1. Meaning and Definition of Control:

According to Koontz and O’Donnel, “The managerial function of control is the measurement and correction of the performance of subordinates in order to make sure that enterprise objectives and the plans devised to attain them are accomplished.”

ADVERTISEMENTS:

According to E.F.L. Brech, “Control, i.e., checking current performance against predetermined standard contained in the plans, with a view to ensuring adequate progress and satisfactory performance, also ‘recording’ the experience gained from the working of these plans as a guide to possible future operations.”

According to Henry Fayol. “Control consists of verifying whether everything occurs in conformity with the plan adopted, the instructions issued and principles established. It has an object to point out weakness and errors in order to rectify and prevent recurrence. It operates on everything- things, people, actions.”

According to G. Terry, “Controlling can be defined as the process of determining what is to be accomplished, that is the standard, what is being accomplished, that is the performance, evaluating the performance and if necessary applying corrective measures so that the performance takes place according to the plans, that is in conformity with the standard.”

Essay # 2. Steps Involved in the Control Process:

ADVERTISEMENTS:

i. Establishment of Standards:

The first step in the control process is to establish standards against which results can be measured. Standards can be defined as, “The criteria of performance or yardsticks which serve as the criteria for judging results.” Standards should be defined as far as possible in quantitative terms to make controlling more specific and accurate.

For example, standards should be measurable in terms of physical units, costs, time, profits, etc. Standards also need to be flexible in order to adapt to changing conditions. For example, a new salesman who poses to be an above average performer should have his sales standard adjusted accordingly. There are many kinds of standards like physical standards, cost standards, revenue standards, capital standards, etc.

ii. Measurement of Performance:

ADVERTISEMENTS:

Once the standards are developed adequately, then the actual performance is to be measured accurately to reveal any variation. Appraisal of performance can be done by personal observation as in case of subordinates being observed while engaged in work and by a study of various summaries or figures, reports and statements.

Accurate and timely measurement of results is dependent on an effective system of reporting. Measurement and reporting of performance may take place at periodic intervals- weekly, monthly, quarterly or yearly.

iii. Comparison of Actual Performance with the Standards:

In comparing performance with the standards fixed, the manager is not only required to find the extent of variation but also the causes of variation. If the actual performance falls short of standards, the management must calculate the extent of deviation.

ADVERTISEMENTS:

The management should be in a position to distinguish between unimportant deviations and important deviations. Focusing on important deviations is known as ‘control by exception’. Whereas, it is waste of time and effort to concentrate on minor deviations.

The next step is to make a detailed analysis to find out the causes of deviations. The deviations may be due to errors in planning, defective implementation or inefficiency in performance.

iv. Correction of Deviations:

ADVERTISEMENTS:

The next step in the process of controlling to be taken by the manager is to correct the deviations between the actual performance and the prescribed standards. Corrective standers should be taken immediately after determining the correct causes of deviations. The management may correct deviations by redrawing their plans or modifying their goals. They may also correct deviations by reassignment of duties, better selection and training of subordinates and change in styles of direction.

Essay # 3. Techniques of Control:

The techniques of control may broadly be classified into the following two categories, namely:

i. Traditional Control Devices, and

ADVERTISEMENTS:

ii. Modern Control Devices.

The Traditional Control Devices can be further sub-divided into:

(i) Budgetary Control Devices and

(ii) Non-budgetary Control Devices like statistical data and reports, breakeven analysis and internal audit.

ADVERTISEMENTS:

There are numerous complicated network techniques of control (i.e. modern device) which are being used by big enterprise, of which PERT and CPM have become very popular.

(i) Budgetary Control:

Budget is an “estimate of future requirements about the activities of the concern for a particular period”, therefore, a process known as Budgetary control is very helpful which is a “process of comparing the actual result with the corresponding budget data to know the actual cause of differences”.

It can also be defined as the process which keeps the actual standards as nearly as possible to the predetermined standard by strict supervision.

Budgetary control is useful to know about the extent of profits or losses being made.

Merits of Budgetary Control:

ADVERTISEMENTS:

The budgetary control has the following advantages to offer:

i. It guides the management in policy-formulation and planning.

ii. It aims at the maximisation of profits through effective cost control, and the proper utilisation of the resources and existing facilities of the business

iii. It increases production efficiency, eliminates wastes, controls the overheads and effects economy in expenditure.

iv. It helps in cost control. The actual performances are compared with the budgeted targets, and control is exercised on the costs.

v. It guides the management in the field of research and development and of future planning.

ADVERTISEMENTS:

vi. It helps the principle of ‘management by exception’ to operate.

vii. It helps in setting standards for the purpose of standard costing, and the comparison made under budgetary control of the actual with the budgets helps in working out the variances under standard costing.

(ii) Non-Budgetary Control:

A. Report for Control:

Management accountant prepares the reports to give information for control and planning.

Certain types of reports that have to be prepared and submitted to management regularly are given as follows:

ADVERTISEMENTS:

(i) Top management:

The reports to be submitted to the top management may relate to:

a) Position of stock.

b) Cash-flow statements.

c) Sales, production and other appropriate statistics.

d) Profit and Loss statement.

ADVERTISEMENTS:

e) Balance Sheet.

(ii) Sales management:

(a) Actual sales compared with budgeted sales to measure performance by products, territories or customers.

(b) Standard profit and loss by products.

(c) Selling expenses in relation to budget and sales value.

(d) Bad debts and accounts that are slow and difficult in collection.

ADVERTISEMENTS:

(e) Status reports on new or doubtful customers.

(iii) Production management:

(a) Price variation on purchases analysed by commodities.

(b) Operational efficiency for individual operators duly summarised as departmental averages.

(c) Scrap report.

(d) Labour utilization report.

(e) Plant utilization report.

(f) Material usages report.

(iv) Special reports:

(a) Taxation legislation and its impact on profits.

(b) Break-even analysis.

(c) Replacement of capital equipment.

(d) Special pricing analysis.

(e) Make certain equipment or purchase it.

B. Break-Even Point:

This techniques was invented by Waler Rautenstraunch. It refers to the point at which the total costs and total revenue are equal and it is only after the attainment of this point that the business can hope to earn profit.

The following studies can be made with the help of the break-even chart technique:

(a) Problems relating to operating policy.

(b) Problems relating to managerial control.

(c) Problems relating to financial administration.

Merits of Break-Even Chart:

They are as follows:

(i) It is a Management Guide. It shows the effect of additional sales on the profits.

(ii) It is the starting point of the virtuous circle. It determines the most profitable price for the products of the enterprise.

Demerits of Break-Even Chart:

The demerits of break-even-chart are as follows:

(i) Cost and revenue should be taken into account to determine the break even-point. The one without the other has no meaning. The total revenue can be kept constant even if the volume of production is less and vice versa.

(ii) Whatever goods are produced, they are immediately sold and yield profit to businessmen. There is a big time lag between production and sales.

(iii) The solutions and allocations of costs in the company are usually arbitrary. This factor too affects the effectiveness of break-even-chart.

Factors like plant-size, technology and methodology of production have to be kept constant in order to draw an effective break-even-chart.

C. Network Technique of Control:

PERT and CPM as Tools of Control:

For a wide range of planning and control problems PERT and CPM are used as techniques of project management. PERT stands for Programme Evaluation and Review Technique while CPM stands for Critical Path Method.

These are needed in basic management functions of planning, scheduling and control. Now a days, business projects are big and complicated. These techniques complete the work within the specified period. Production delays and conflicts are minimised. The coordinate the various jobs of the total project and thus complete the entire job to scheduled period.

Essential Steps in using PERT and CPM:

These are as follows:

(i) All the independent jobs of project should be separately listed.

(ii) The order of precedence for doing the jobs should be determined. To link the whole certain jobs are to be done before. All such relationships between the different jobs or activities should be pre-planned and clearly laid down.

(iii) In this step, graph or picture is drawn to show the performance of the different activities and their relationship. It will deal with priority of the jobs and the required time for its completion. It can be called ‘project graph’ or arrow diagram’.

Project Graph:

In the project graph, the different activities are shown by way of arrows leading from one circle to another. Arrow connecting the two circles represent a job.

It is essential to locate the longest path of sequence connecting the different activities through the net-work. This is known as ‘critical path’ of the project.

The different activities involved in the preparation of the budget may be listed as given in the budgeting activities of the firm.

Essay # 4. Importance of Controlling:

It is impossible to imagine any organisation completely devoid of control as an integral part of its system. Control is necessary for an organisation to achieve its objectives. Changing environment of organisations, increasing complexity of organisational structure and the need of the managers to delegate authority are some of the factors which make control a necessity in today’s organisation.

The importance of control arises from the points given below:

i. Execution of Plans:

The risk of non-conformity of actual performance with intended goals is largely eliminated by an important element of management. The major function of control lies in regulating operations in such a way as to insure the attainment of predetermined purposes.

ii. Extension of Decentralisation:

The control system has encouraged top management to extend the frontiers of decentralisation without losing ultimate control in a number of ways. Control becomes absolutely necessary to make certain the efficient functioning of these decentralised units.

iii. Simplifies Supervision:

Control helps to simplify the tasks of the supervisor by identifying significant deviation from the set standards. This enables the supervisor to take corrective measures before any major losses occur to the business due to in effective supervision.

iv. Facility of Co-Ordination:

Co-ordination is facilitated by control function of management. Control keeps all activities and efforts within their fixed boundaries and schedules, and it makes them to move towards common objectives through co-ordinated directives. All wastes of times, money and efforts can be avoided through the control function of management.

v. For Corrective Action:

The control measurements and reports serve little purpose unless corrective action is taken when it is discovered that current activities are not leading to the desired results.

vi. Indication of Managerial Weakness:

The control function of management reveals and feeds back necessary information for indicating managerial weakness and taking necessary remedial actions.

Essay # 5. Characteristics of Good Control System:

i. Appropriate:

The control system should be appropriate to the nature and needs of a concern and each level of activity inside it. If the control system is not upto the mark, then the deviations of actual performance and standard performance may not give a correct and desired result.

ii. Flexible:

Control must be flexible so as to accommodate all changes of failures in plans. If plans are required to be revised for attainment of objectives, the control system must have the attribute of adjusting itself to changed circumstances.

iii. Simple:

A good control system must be easy to understand. A complicated control system will not only create difficulties in the proper performance of activities, but will also not give the desired results.

iv. Economical:

A good control system should be economical. In other words, it should be easily installed and inexpensively maintained.

v. Strategic Control Points:

Control is to be exercised on strategic points. The best selection of strategic control points implies effective controlling at a minimum of cost and effort. To attempt to control everything is to betray the main objective of controlling.

vi. Easy Comparison:

A control system can be said effective only when past performance is easily comparable with standards, otherwise control system is said to be defective.

vii. Quick Reporting:

Control must report deviations quickly. This will ensure quick action to set things right. If this characteristic is not found in any control system it is said to be defective.

viii. Qualified Staff:

If the control system has qualified staff to attain the objectives, only then it can be said effective. In the absence of qualified and competent staff, it will not be an easy job to have control on all the activities of the firm.

ix. Ensure Corrective Action:

A good control system must ensure corrective action. It should not only detect deviations and failures, but should also disclose where they are occurring, the man responsible for them and what should be done to correct them.

Essay # 6. Limitations or Shortcomings of Control System:

The control system has a number of limitations, which are given below:

i. Lack of Satisfactory Standards:

There are many activities involving intangible performance for which no satisfactory standards can be established. For example, results of management development, human relations, public relations, research, etc. cannot be accurately indicated by any pre-determined standard.

ii. Human Reactions to Control:

Of all functions of management, control invites greater opposition from subordinates because of its interference with their individual actions and thinking. If the system of control is of the close and detailed type, it is likely to create adverse morale effects among lower-level managers.

iii. Imperfections in Management:

Intangible performance creates difficulties not only in case of establishing standards, but it also complicate the task of measuring results for evaluation. Moreover, measurement of all results of everybody’s work is not feasible on economy considerations.

iv. Limitations of Corrective Action:

There are several limitations in taking corrective actions and avoiding mistakes. Managerial mistakes of studying market demand are only known consequently when products are put on the market. Moreover, lack of authority and of timely control information may make some corrective actions beyond the scope of controlling.

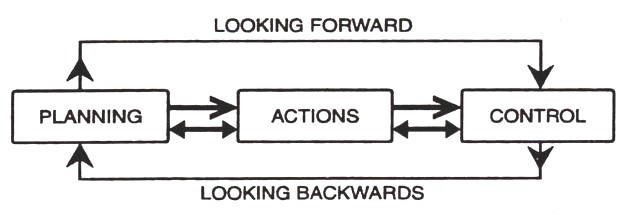

Essay # 7. Relationship between Planning and Controlling:

A good definition of management control is, “The process through which the managers assure that the actual activities conform to planned activities.” While planning an organisation’s activities, the fundamental goals, objectives and the methods for attaining them are established.

The controlling process measures the progress of the organisation towards attainment of these goals and enables managers to detect deviations from the plan in time to take corrective actions before it’s too late.

Thus, planning and controlling may be valued as the two blades of a pair of scissors, that is one cannot work without the other. Without objectives and plans, control is not possible because performance has to be compared against some established criteria. On the other hand, planning is fruitful only when there is effective control.

In the words of B.E. Goetz, “Managerial planning seeks consistent, integrated and articulated programmes. One management control seeks to compel events to conform to plans.”

Planning and controlling are thus correlated and facilitate effective decision-making. The control process helps to reveal the defects in the standards established leading to revision in plans, setting of new goals, changes in organisational structure and improvement in staffing and techniques of direction. In this way controlling ensures better coordination amongst the functions of management.

Managerial planning which involves determination of objectives, strategies, standards, provides the basis of controlling activities. Thus, control has no basis without planning just as planning is meaningless without control. To sum up, controlling and planning are inter-dependent and complementary.