Here is a term paper on ‘Dividend’. Find paragraphs, long and short term papers on ‘Dividend’ especially written for school and college students.

Term Paper on Dividend

Term Paper Contents:

- Term Paper on the Meaning of Dividend

- Term Paper on the Determinants of Dividend Policy

- Term Paper on the Tax Considerations in Dividend Decision

- Term Paper on the Constant Dividend Rate Policy

- Term Paper on the Variants of Constant Dividend Policy

- Term Paper on the Optimum Dividend Policy

- Term Paper on the Dividend Models

- Term Paper on Modigliani and Miller’s Dividend Irrelevancy Theory

1. Term Paper on the Meaning of Dividend:

ADVERTISEMENTS:

The prime objective of a firm is to maximize wealth of its owners i.e., shareholders.

Cash inflows are generated from the successful operation of business which are used for payment of dividends to its shareholders. Dividend paid represents a cash outflow which depletes the cash resources.

The dividend decision is regarded as a financing decision since any cash dividend paid reduces the amount of cash available for investment by the firm.

Dividends are periodic cash payments by the company to its shareholders.

ADVERTISEMENTS:

The dividend payable to the preference shareholders is usually fixed by the terms of the issue of preference shares.

But the dividend on equity shares is payable at the discretion of the Board of Directors of the company.

For payment of dividends, a company must earn distributable profits from which the actual payment of dividends will be made.

Dividend policy is contemporary to retention policy. Retentions are used to finance capital projects and redeem shares and debentures.

ADVERTISEMENTS:

ADVERTISEMENTS:

2. Term Paper on the Determinants of Dividend Policy:

Dividend policy determines the distribution of net cash flows generated from successful trading between dividend payments and corporate retentions.

1. Transaction Costs:

The transaction costs are of two different types:

ADVERTISEMENTS:

i. Firm’s Transaction Costs:

The costs incurred in raising new capital are called ‘flotation costs’ and it is ranging as high as 10% of the amount raised. The flotation costs associated with raising new funds give firms an incentive to avoid paying dividends.

ii. Shareholders Transaction Costs:

When a stock is sold, the investor must pay transaction costs of approximately 1-2% of the share’s value. The firm may be able to provide investors with dividend income at a lower transaction cost than if the investors provided income for themselves.

ADVERTISEMENTS:

2. Dividend Clientele:

Firms with different dividend policies will appeal to different kinds of investors, with each group constituting a different dividend clientele. A dividend clientele is a group of investors favouring a particular kind of dividend policy. Low and zero taxpayers appear to prefer high payout ratios, while high taxation groups prefer low dividends and expect to realize benefits through capital gains.

3. Dividend Payout Ratio:

Determination of dividend payout ratio is one of the major financial decisions effecting the firm’s wealth as well as market price of the share. Dividend payout ratio represents the percentage of dividend declared and paid out of the earnings per share.

![]()

Dividend payout indicates the extent of the net profits distributed to the shareholders as dividend. A high payout ratio signifies a liberal distribution policy drives down the cash resources available with the company. A low payout ratio indicates conservative distribution policy, which enables the firm to accumulate internal resources for future capital expenditure, growth and diversification, which will result in long-run capital appreciation of share price and maximization of firm’s wealth.

4. Dividend Cover:

The dividend cover is calculated as follows:

![]()

This ratio indicates the number of times the dividends are covered by net profit. This highlights the amount retained by a company for financing its future operations.

ADVERTISEMENTS:

5. Dividend Signalling:

Changes in dividend policy may convey information to the stock market. An increase in dividends is likely to be interpreted as ‘good news’ and a cut as ‘bad news’. The complete skip- off of a dividend is likely to be regarded as very bad news. The companies use this information channel to inform the investors.

6. Divisible Profits:

All the profits of a company are not divisible. Only those profits which can be legally distributed in the form of dividend to the shareholders of the company are called as ‘divisible profits’, otherwise, it is treated as payment of dividend out of capital and the directors of the company are liable to make it good.

7. Liquidity:

ADVERTISEMENTS:

In order to pay dividend, a company requires cash and, therefore, the availability of cash resources within the company will be a factor in determining dividend payments. The liquidity position of the company will influence the dividend payout of a particular year.

8. Rate of Expansion:

The rate of asset expansion needs to be taken into account. The more rapid the rate at which the firm is growing, the greater will be its needs for financing asset expansion. The greater the future need for funds, the more likely the firm is to retain earnings rather than pay them out.

9. Rate of Return:

Profit rate influences the dividend/retention policy. The rate of return on assets determines the relative attractiveness of paying out earnings in the form of dividends to shareholders who will use them elsewhere, compared with the productivity of their use in the present enterprise.

10. Stability of Earnings:

ADVERTISEMENTS:

The stability of earnings also effects the decision. If earnings are relatively stable, a firm is better able to predict what its future earnings will be. A stable firm is, therefore, more likely to pay out a higher percentage of its earnings than is a firm with fluctuating earnings.

11. Stability of Dividends:

The stability of dividends ensures the consistency of future stream of income to the shareholders, Small shareholders generally do not prefer variability in their future earnings in the form of dividends, they require a stable dividend policy,

12. Legal Provisions:

The company has to comply with the provisions of the Companies Act, 1956 for payment of dividends. As per the provisions, the company must earn distributable profits from which the actual payment of dividends are made. A company must transfer a certain percentage of profits of current year to reserves, before declaring a dividend.

13. Contractual Constraints:

ADVERTISEMENTS:

When the company obtained loan funds from debenture holders or term lending institutions, the terms of issue or contract of loan may contain restrictions on dividend payments designed to ensure that the firm will have enough funds to meet its obligations to the loan providers.

14. Cost of Financing:

The cost of external financing will have impact on the dividend payout of a company. In situations where the external funds are costlier, a firm may resort to low dividend payout and use the internal funds for financing its business.

15. Degree of Control:

The management who wish to maintain close control over the firm will not much depend on the external sources of finance, and they maintain a low dividend payout policy and the funds generated from operations would be used for working capital and capital investment needs of the firm.

16. Capital Market Access:

ADVERTISEMENTS:

A firm intends to raise further funds from the capital market for its expansion and diversification projects, to attract the funds from the capital market, it has to maintain a liberal dividend policy.

3. Term Paper on the Tax Considerations in Dividend Decision:

The tax considerations in the context of a dividend decision of a company can be looked into the following angles:

1. Corporate Taxation:

The dividend on shares is an appropriation of profits. The declaration of dividend will be made from after tax profits. Therefore, a dividend payment will have least effect on corporate taxation.

2. Personal Taxation:

ADVERTISEMENTS:

Dividend payments to individuals are subject to personal taxation in the year received. At the time of selling the shares, the investor will be attracted with capital gains. By paying dividends, a corporation is forcing its stockholders to have to pay taxes earlier than they would if the dividends were not paid.

Constant Dividend Payout Policy:

This method is also known as ‘constant payout ratio method’.

Stability of dividends means ‘always paying a fixed percentage of the net earnings every year’.

Under this method, if earnings vary, the amount of dividends also varies from year to year.

The dividends varies from year to year, if earnings vary.

The dividend policy is entirely based on company’s ability to pay under this policy.

The company follows a regular practice of retained earnings.

For most firms, earnings are quite volatile, fluctuating with changes in the economy and firm’s own special circumstances.

Very few firms select this method.

The relation between earnings per share and dividend per share under this policy is shown in Figure 5.1.

4. Term Paper on Constant Dividend Rate Policy:

The relation of earnings per share and dividend per share under this policy is shown in Figure 5.2.

It is a most popular kind of dividend policy which advocates the payment of dividend at a constant rate, even when earnings vary from year to year.

This may be possible only when the earnings pattern of the company does not show wide fluctuations.

This policy is possible only through the maintenance of what is called ‘dividend equalization reserve’.

The company then invest funds equal to such reserves in some current investments so as to manage the liquidity of the necessary funds in times of need.

Firms are generally careful to set the dividend at a sustainable level and raise it only when the firm can sustain the higher level.

Occasionally firms may cut dividends in adverse situations.

Firms are against cutting dividends, because of the extremely unfavourable news it conveys to the market.

5. Term Paper on the Variants of Constant Dividend Policy:

1. Multiple Dividend Increase Policy:

Some firms follow a policy of very frequent and very small dividend increases to give the illusion of movement and growth. The obvious hope behind such a policy is that the market rewards consistent increases.

2. Regular Dividend plus Extra Dividend Policy:

Some firms consciously divide their announced dividends into two portions a regular dividend and an extra dividend. The regular dividend is the dividend that will continue at the announced level. The extra dividend payment will be made as circumstances permit.

3. Uniform Cash Dividend plus Bonus Shares Policy:

This policy is usually adopted in case of companies which have fluctuating earnings. Under this method, a minimum rate of dividend per share is paid in cash plus bonus shares are issued out of accumulated reserves. But the issue of bonus shares is not on annual basis. It depends upon the amount kept in reserves over a period.

6. Term Paper on the Optimum Dividend Policy:

Accepting that there is an optimum dividend policy, it is then necessary to find an approach to decide what the payout ratio should be. One approach would be to assess the net preferences for dividends over capital gains, this is illustrated in Figure 5.3.

In Figure 5.3 Curve A shows how the share price is likely to vary with the size of pay-out ratio. Curve B shows the effect of higher payout ratios in reducing share values. This reduction of share values is due to the fact that higher pay-out require that outside funds be obtained to replace the dividends paid. Curve C shows the combined influences of these two factors on share price. If the company does not have sufficient investments to use up all its earnings, the residue should be earmarked for payment as dividends.

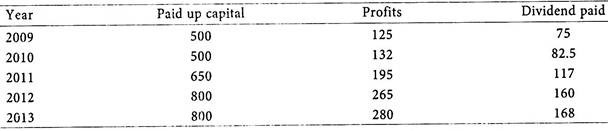

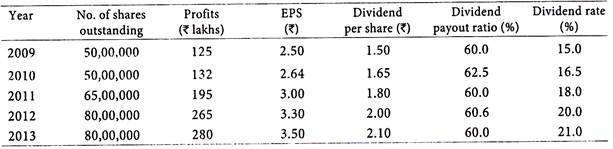

Illustration:

Tourist Resorts Ltd. is a listed company paying dividends every year.

Its last five-year profit and dividend track record is given below:

Analyze the company’s dividend policy.

Solution:

Calculation of EPS.

Analysis – From the above analysis we can understand that the company is maintaining a constant dividend policy consistently by paying out 60% of the profits earned, to the equity shareholders. We can also observe that the company is increasing its dividend based on the increase in profits year after year.

7. Term Paper on Dividend Models:

1. Gordon Growth Valuation Model:

The dividends of most companies are expected to grow and evaluation of value shares based on dividend growth is often used in valuation of shares.

Dividend valuation model assumes a constant level of growth in dividends in perpetuity.

The Gordon growth model is a theoretical model used to value ordinary equity shares.

The model incorporates the retention of earnings and growth of dividends and hence it is also called as ‘dividend growth valuation model’.

The main proposition of the model is that the value of a share reflects the value of the future dividends accruing to that share. Hence, the dividend payments and its growth are relevant in valuation of shares.

The model holds that share’s market price is equal to the sum of share’s discounted future dividend payments.

In valuation of share under Gordon growth model, the following formula is used:

![]()

Where,

P0 = Current ex-dividend market price of share

D0 = Current year’s dividend

D1 = Expected dividend

Ke = Cost of equity capital i.e. expected rate of return on equity capital

g = Expected future growth rate of dividends

The shareholders’ required rate of return (Ke) can also be calculated by using the capital asset pricing model. The model requires the estimation of future growth of dividends.

The Gordon Growth Model using dividend capitalization can also be presented as follows:

![]()

Where,

P0 = Current ex-dividend market price of share

E1 = Expected earnings per share

b = Retention ratio

(1 – b) = Dividend payout ratio

Ke = Cost of capital or Capitalization rate

br = g = Growth rate of earnings and dividends

Assumptions of Gordon Growth Valuation Model:

The model using dividend capitalization is based on the following assumptions:

1. The firm is an all-equity firm and has no debt.

2. External financing is not used in the firm. Retained earnings represent the only source of financing.

3. The internal rate of return is the firm’s cost of capital ‘k’. It remains constant and is taken as the appropriate discount rate.

4. Future annual growth rate dividend is expected to be constant.

5. Growth rate of the firm is the product of retention ratio and its rate of return.

6. Cost of capital is always greater than the growth rate.

7. The company has perpetual life and the stream of earnings are perpetual.

8. Corporate taxes does not exist.

9. The retention ratio ‘b’, once decided upon, remains constant. Therefore, the growth rate g = br, is also constant forever.

Criticism on Gordon Growth Model:

1. In real world, the constant dividend growth and earnings growth is a fallacy.

2. The model implies that if ‘D0‘ is zero, the value of share is nil.

3. The capital gains are ignored by the model.

4. The false assumption is that investors will buy and hold the shares for an infinite period of time.

5. The model ignores the allowance for corporate and personal taxation.

6. The diminishing marginal efficiency of investment is ignored.

7. The effect of change in the firm’s risk-class and its effect on firm’s cost of capital is ignored.

Illustration 1:

Royal Products Ltd. is an established company having its shares quoted in the major stock exchanges. Its share current market price after dividend distributed at the rate of 21% p.a. having a paid up share capital of Rs.50 lakhs of Rs.10 each. Annual growth rate in dividend expected is 3%. The expected rate of return on its equity capital is 16%.

Calculate the value of Royal Products Ltd.’s share based on dividend growth model.

Solution:

Dividend Distributed During the Year = Rs.50,00,000 × 21/100 = Rs.10,50,000

![]()

Value per share = Rs.83,19,231/5,00,000 equity shares = Rs.16.64

2. Walter’s Valuation Model:

Prof. James E. Walter argued that in the long-run the share prices reflect only the present value of expected dividends. Retentions influence stock price only through their effect on future dividends. Walter has formulated this and used the dividend to optimize the wealth of an equity shareholder.

His formula in determination of expected market price of a share is given below:

P = {[D + Ra /Rc (E – D)]/Rc}

Where, P = Current market price of equity share

E = Earnings per share

D = Dividend per share

(E – D) = Retained earning per share

R = Rate of return on firm’s investment

Rc = Cost of equity capital

If Ra/Rc is greater than 1, lower dividend will maximize the value per share and vice versa.

Assumptions of Walter’s Valuation Model:

1. All financing is done through retained earnings and external sources of funds like debt or new equity capital are not used. Retained earnings represent the only source of funds.

2. With additional investment undertaken, the firm’s business risk does not change. It implies that firm’s IRR and its cost of capital are constant.

3. The return on investment remains constant.

4. The firm has an infinite life and is a going concern.

5. All earnings are either distributed as dividends or invested internally immediately.

6. There is no change in the key variables such as EPS and DPS.

Walter’s model recognizes the importance of IRR, and cost of capital for valuation of share and dividend decisions. The Walter’s model is applicable to all-equity firms.

Implications of Walter’s Model:

(i) The optimum dividend policy of a firm is determined by the relationship of ‘Ra‘ and ‘Rc‘.

(ii) If Ra > Rc i.e., if the firm can earn higher IRR than the cost of capital, the firm can retain the earnings. Such firms are called as ‘growth firms’ and their dividend policy would be to plough back the earnings. The optimal payout ratio for a growth firm is nil. In a company when the rate expected by investors (Rc) is higher than market capitalization rate (Ra), shareholders would accept low dividends. When the rate of return on investments (Ra) exceeds the cost of capital (Rc), the price per share increases as the dividend payout ratio decreases.

(iii) If Ra < Rc i.e., the cost of capital is more than firm’s IRR or when the firm does not have profitable investment opportunities, the optimum dividend policy would be to distribute the entire earnings as dividend. Such firms are called ‘declining firms’. The optimal payout ratio for a declining firm is 100%.

In a company where return on investment (Ra) is lower than market capitalization rate (Rc), shareholders would prefer higher dividend so that they can utilize the funds so obtained elsewhere in more profitable opportunities. When the rate of return on investment (Ra) is less than cost of capital (Rc), the price per share increases and the dividend payout ratio increases.

(iv) If Ra= R i.e., if IRR of the firm is equal to its cost of capital, it does not matter whether the firm retains or distribute its earnings, such firms are called ‘normal firms’ and its optimal payout ratio is irrelevant. When the rate of return on investment (Ra) is equal to cost of capital (Rc), the price per share does not vary with changes in dividend payout ratio.

Thus, according to him, the investment policy of a firm cannot be separated from its dividend policy and both are interrelated. The choice of an appropriate dividend policy affects the value of an enterprise. Retentions influence the share prices only through their effect on further dividends. Walter’s formula is criticized for the reason that it does not consider all the factors affecting dividend policy and share prices.

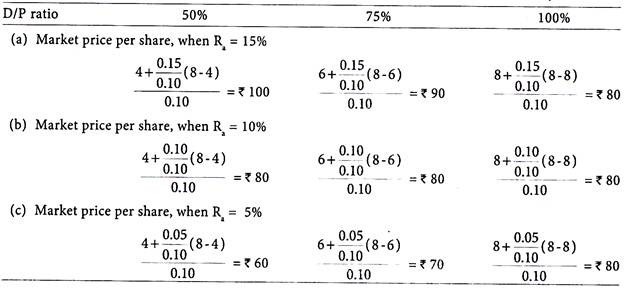

Illustration 2:

The earnings per share of a company is Rs.8 and the rate of capitalization applicable is 10%. The company has before it an option of adopting (i) 50%, (ii) 75% and (iii) 100% dividend payout ratio. Compute the market price of the company’s quoted shares as per Walter’s model if it can earn a return of (a) 15%, (b) 10% and (c) 5% on its retained earnings.

Solution:

Computation of Market Price of Company’s share by applying Walter’s Formula:

P = {[D + Ra /Rc (E – D)]/Rc}

Where, P = Current market price of equity share

E = Earnings per share i.e., Rs. 8

D = Dividend per share.

Ra = Internal rate of return on investment

Rc = Cost of equity capital i.e., 10% or 0.10

Now, we can calculate the Market Price per Share based on Different IRRs and Dividend Payout Ratios.

8. Term Paper on Modigliani and Miller’s Dividend Irrelevancy Theory:

Modigliani and Miller has argued that a firm s dividend policy has no effect on its value of assets.

For example, if the rate of dividend declared by a company is less, its retained earnings will increase and so also the net worth and vice versa.

Their argument is that the value of the firm is unaffected by dividend policy i. e., dividends are irrelevant to shareholders wealth.

MM-Dividend Irrelevancy Theory is based on the following tenets:

1. Investment Policy:

MM argue that a firm’s value is determined solely by its investment decisions and that the dividend payout ratio is a mere detail. They believe that the firm’s investment policy is not affected by its dividend policy. According to them, the share valuation is independent of the level of dividend by the company.

2. Earning Power:

MM asserts that the value of the firm is determined by its basic earnings power and its risk class, and therefore, the firm’s value depend on its asset investment policy rather than how earnings are split between dividends and retained earnings.

3. Signalling Effect:

MM pointed out that investors are indifferent as to the manner in which the returns are obtained, dividends or capital gains. The changes in dividend payments represent a signal to investors concerning management’s assessment of the future earnings and cash flows of the company.

4. Information Content:

A change in dividends has an effect on price of firm’s stock is related primarily to ‘information about future earnings conveyed by a change in dividends’. The increase in cash dividends raise expectations about the level of future earnings.

5. Clientele Effect:

MM states that a firm will attract stockholders whose preferences with respect to the payment pattern and stability of dividends corresponds to the firm’s payment pattern and stability of dividends.

Market price of a share, after dividend declared, is calculated by applying the following MM formula:

![]()

Where, P0 = Prevailing market price of a share

P1 = Market price of a share at the end of period one

D1 = Dividend to be received at the end of period one

Ke = Cost of equity capital

The number of shares to be issued to implement the new projects is ascertained with the following formula:

![]()

Where, ΔN = Change in the number of shares outstanding during the period (i.e. number of new shares to be issued)

I = Total investment amount required for capital budget

E = Earnings of net income of the firm during the period

n = Number of shares outstanding at the beginning of the period

D1 = Dividend to be received at the end of period one

P1 = Market price of a share at the end of period one

Assumptions of MM Dividend Irrelevancy Theory:

MM built their argument on a number of assumptions, the most important of which were:

1. There are no personal or corporate income taxes.

2. There are no stock flotation costs, transaction costs and brokerage fees.

3. Dividend policy has no effect on the firm’s cost of equity.

4. The firm’s capital investment policy is independent of its dividend policy.

5. Investors and managers have equal and cost less access to information (symmetric information) regarding future opportunities.

6. All investors can lend or borrow at the same rate of interest.

7. No buyer or seller of securities can influence prices.

8. Dividend decisions are not used to convey information.

9. Perfect capital market exists with free flow of information.

10. Investors behave rationally, they try to increase their income and wealth and are indifferent to the form in which a given increase to their income or wealth takes place viz., dividend or capital gain.

11. No tax differential between distributed and undistributed profits as also between dividends and capital gains.

12. Investment opportunities and future net income of all companies are known with certainty to all market participants.