Some frequently asked exam questions on strategic planning are as follows:

Q.1. Give the meaning and definition of strategic planning.

Ans. Strategic Planning is basically a policy-making function.

It is concerned with:

(i) Defining the corporation’s purpose,

(ii) Defining the composition of its business mix, and

(iii) Defining the qualitative and quantitative projection of its achievement (i.e., short-and long-term corporate objectives).

In a word, ‘strategic planning articulates goals, deliberates policy issues and assumes the company’s capacity to achieve’.

In the years after World War II, many of the factors on which earlier planners counted could no longer be taken for granted. Uncertainly, instability, and changing environments became the rule rather than the exception. The managers of business organisations faced increased inflation and intensifying foreign competition, technological obsolescence and changing market and population characteristics.

These changes were so rapid that they exerted an increased pressure on top management to respond. In order to respond more accurately, on a more timely schedule, and with a direction or course of action in mind, the managers are increasingly turning to the use of strategic planning.

Various definitions have been given to ‘strategic planning’ by various scholars. Some of them are:

1. Strategic Planning refers to the development of strategic plans that involve taking information from the environment and deciding upon an organisational mission, and upon objectives, strategies, and a portfolio plan (Rosenberg and Schewe, Business Horizons, 1987).

2. Strategic Planning involves establishing the overall identity of the company, deciding on the strategic alternatives the company will follow, and choosing the tactics or weapons which the company will emphasize (Galkrevth, Jay).

3. Strategic Planning is a process that involves the review of market conditions; customers’ needs; competitive strengths and weaknesses; socio-political, legal, and economic conditions; technological developments; and the availability of resources that lead to the specific opportunities or threats facing the organisation (Gibson and Ivancevich, 1990).

Simply put, strategic planning involves identifying the long-term objectives and determining the action plans for the company. The objectives and action plans should be established only after careful assessment and prediction of the future states of relevant environmental factors.

Case Examples:

1. ABC Co. Ltd. decided to develop a new technology and planned to achieve dominance in this new area by utilising the distribution channels and sales forces of several established companies. It also decided to rely on outside suppliers for most component parts and on another manufacturer for final assembly.

If demand developed as the company anticipated, consideration would be given to developing the company’s own assembly plant, although most component parts would continue to be purchased during the foreseeable future.

Funds were to come from three sources:

(i) Initial limited financing from the owner-founder,

(ii) Subsequent inflow of debt and equity by the company undertaking the final assembly, and

(iii) Subsequent offerings of equity to the public.

The preceding statement delineates the basic strategic plan for ABC Co. Ltd. The plan, here, was a high-risk one since the company knew that other larger companies were developing competing technologies. It was, therefore, a race to see who made it to the market first.

2. DEF Co. Ltd. decided to commit itself to maintaining a long established tradition of unexcelled quality product.

Its basic strategic plan is as follows:

(i) The company produces a limited number of products of unexcelled quality;

(ii) The production is carried out by highly skilled craftsmen;

(iii) Some limited automation is introduced each year but only after extensive testing to assure maintenance of superb quality;

(iv) The company makes most of the component parts in its own factory and tests each product for a significant period of time after completion;

(v) All rejected pieces are disassembled, no second-quality units are sold;

(vi) The company’s small sales force serves a set of limited and carefully selected distribution outlets, most of which have well-established names of their own, only one or two outlets are added each year and these only when another outlet has ceased operation;

(vii) The company carries out limited advertising in magazines and T.V. normally read and seen only by upper-level socio-economic classes; and

(viii) The ownership is held by the fifth generation of the family, and recently, a portion of ownership was given to the first non-family member who assumed the position of managing director.

The above two case examples reflect two strategic descriptions for two different companies. Yet, they fulfil the basic issues given in the definitions of strategic planning.

Q.2. What are the advantages of strategic planning?

Ans. A formal strategic planning offers the following advantages:

1. A spirit of creativity and initiative in the managerial personnel.

2. An awareness about the external environmental variables particularly the areas of risk and uncertainty, and opportunities and threats.

3. A guide for existing and future parameter for functional and project managers to direct their actions on the courses of action charted by the top executive.

4. An in-built benchmark to compare the actual performance with projections.

5. A basis for review and replacement of old paradigms by new ones and new skills to be adopted by a forward-looking organisation.

Q.3. A strategy is said to be similar to the concept of a ‘Game Plan’; but it is not exactly the same. Discuss.

Ans. Some business management writers borrowed from the game plan or theory to define strategy as a set of specific product-market entries, while others have defined it in the military sense as the broad overall concept of the firm’s business.

A strategy is similar to the concept of a game plan in the sense that both are concerned with using and optimising the resources available with each. A coach of a team in a game examines the opponent’s plans, strengths, weaknesses, etc., and his objective is to win the game.

But a game plan or theory is not exactly a strategy or vice-versa. A game plan is oriented against a particular competitor — player or a series of players in succession; that is, series of games. But a strategy of a firm is a long-term plan and has to consider a number of competitors.

Even if a strategy of a firm is compared with a football game plan where the number of players are many like that of competitors to a firm, we find the analogy incomplete. Such game-plan has no external constraints like the constraints with respect to government control, suppliers and others found with a business firm.

A coach may have an excellent game plan but the game is played on the field by the players. For successful performance of a firm, a unified and an integrated plan assumes the roles of operational executives. As a tool for solution of business problems, game theory has achieved limited success.

Game theory, being a mathematical technique helpful in planning in situations of conflict, suffers from the fact that the mathematical part is still capable of solving only very elementary games and has failed to construct a total approach towards solution of more than a few ‘games’ of practical value, ‘While still far from being a practical management tool, game theory offers an extremely powerful and useful concept for analysis of strategic problems in which interactions among the competitors has a strong influence on strategy’.

To conclude, we can say that if any of the product-market scope alternatives do pose major competitive implications, they should be examined from the viewpoint of game theory.

This helps to define and recognise the counter-strategies which the competition may call for. As a result of such study, the respective ratings and hence the ranks of the product-market alternatives should be adjusted.

Q.4. What is strategic planning?

Ans. 1. The definitions given hereinbefore clearly indicate that strategic planning is a process. It is a process of deciding in advance what is to be done, when it is to be done, how it is to be done, and who is going to do. It is also a continuous process.

2. Strategic planning is a philosophy and more of a thought process; an intellectual exercise than a prescribed set of and seek to learn what opportunities and threats they face. For example, a consumer goods manufacturer (say, Lakme) may face increasing population in the key age group along with increasing income—this provides an opportunity for sales growth. A threat perceived by the leather companies several years ago was VIP briefcases (leather substitute).

The firm’s top management also looks inside the firm and tries to determine their comparative advantages and weaknesses. Thus Proctor and Gamble’s comparative advantages include very strong consumer marketing, while Lockheed’s weaknesses include inadequate financing.

The top management then tries to match up the opportunities and threats with its own strengths and weaknesses and, on this basis, chooses one of several strategic alternatives, like stable growth strategy or retrenchment strategy or combination strategy.

3. Comprehensive strategic planning may be defined as a structure of plans—a structure that integrates strategic issues with short-range operational plans and into which are integrated, at all levels, major objectives, strategies, policies process, procedures, structures or techniques and functions for a firm.

Q.5. Explain the two types of concept of strategy.

Ans. The two types are : pure strategy and grand or mixed strategy. Pure strategy is a move or a specific series of moves by a business firm, such as product development programme in which successive products and markets are clearly delineated.

A grand or mixed strategy is a statistical decision rule for deciding which particular pure strategy the firm should select in a particular situation.

Q.6. Explain the terms first-generation planning and second-generation planning.

Ans. First-generation planning is one which is considered to be fixed in nature and refers to one which is prepared on the assumption that external and internal environmental variables are stable, and this is preferred by people who like well-defined roles rather than challenging roles.

Second-generation planning is, on the contrary, variable in nature and assumes environmental conditions as variables and unstable, and this is liked by people who prefer variety, dynamism and stimulation.

Q.7. Distinguish between programmed strategy and contingency strategy.

Ans. A ‘Programmed strategy’, usually made at the stage of first-generation planning, consists of strategies planned and detailed so as to follow it all through the implementation phases and does not take into account the changes in the environmental variables during it. The managers and executives who prefer well-defined roles like this strategy.

A ‘contingency strategy’, generally called a second-generation planning and strategy, is flexible enough to accommodate changes and environmental variables. This strategy requires the corporate planner to choose a strategy that is suitable and useful under the best estimates of environmental conditions and other strategic choices. The people having vision and dynamism prefer this strategy.

A contingency strategy is always practical and situation-oriented. A SWOT analysis is a regular exercise in this type of strategy.

Q.8. Differentiate between ETOP and SAP.

Ans. ETOP stands for Environmental Threat and Opportunity Profile and SAP for Strategic Advantage Profile. Both ETOP and SAP are considered together as a diagnostic tool to understand and draft the future business conditions under most probable and worst- case assumptions relating to the external threats and opportunities on certain factors. These two profiles are prepared separately and then matched to determine strategic choices.

The underlying idea of SAP is, thus, to match a firm’s capabilities with opportunities and to introduce strategic input alternatives that may be advantageous to combat threats. There are two basic ingredients in this process : estimation and calculation.

The pre-requisites of sound estimation are : intelligent consultation, thorough understanding of intensity of competition, arid objective assessment of market and product-market characteristics. In contrast, calculation is the art of comparing and risk-taking on those areas where a firm can seek competitive advantages based on its objectivity, preparatory action and decision postures.

ETOP discloses the most critical factors and their potential impact on a firm’s strategy and operations, whereas SAP identifies specific advantages necessitating a firm’s strategic actions.

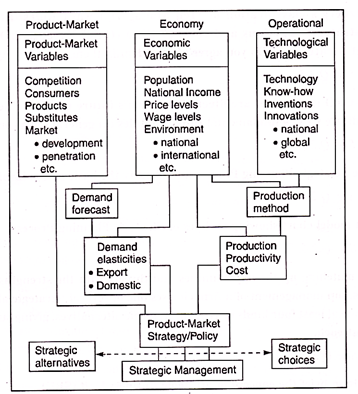

Q.9. Distinguish between operational and strategic management.

Ans. The chart below shows how the marketing management and operational management can come together to devise the product-market strategy for the firm that meets the objectives of consumers, business firms and strategic choices.

The chart exemplifies that strategic management concept is wider and includes operational management. Operational management refers to the management of activities that take place in the form of business functions like production, sales, finance, personnel, etc.

In short, there are two types of management in an organisation—strategic management that exists at the top and all other management might be called operational management. The thought processes, the attitudes, the perspective, the frames of reference, the methods of analysis, and the skills differ between the two.

In essence, strategic management concept has its focus on top management strategic activities in contrast to more routine operational management. This is a new perspective that highlights the importance, in both theory and practice, to a company of this process as well as its uniqueness compared with other managerial functions.

Q.10. Explain the term situational design.

Ans. An effective strategic planning system is unique to the corporate environment in which it operates. Situational design refers to the fact that each corporate enterprise is unique in its various dimensions such as diversity of operations, industry, arid strategy. The personalities of people, organisational culture or value systems, homogeneous, characteristics of the management and orientation to the real world are some of the important elements of situational design necessary for a planning system.

Q.11. The name of strategic planning game is to translate strategy into current decisions. —Comment.

Ans. Basically long-range planning looks at the chain of cause-and-effect consequences over time of an actual or intended decision. Such planning looks at the alternative courses of action that are open in the future and when choices are made, they become the basis for making current decisions. The essence of strategic planning is the systematic identification of opportunities and threats that lie in the future which, in combination with other relevant data, provide a basis for management to make better current decisions to exploit the opportunities and avoid the threats.

Q.12. Write a short note on freewheeling opportunism.

Ans. ‘Freewheeling opportunism’, in a rigid sense, is neither a strategy nor a system but refers to an approach whereby a firm exploits opportunities as and when they arise in the external environment of a business. It is, thus, not a part of formal strategic planning. A firm having no or very little planning framework pursues this approach, in a specific situation, based on its merits.

This approach has both advantages and disadvantages.

Its advantages are :

(1) flexibility and adaptability to any change in the environment;

(2) quick response to situational opportunities;

(3) possibility of short-term gain; and

(4) lower-level managers find interest which a formal planning system does not encourage.

Its disadvantages are :

(1) an opportunity, without adequate appraisal from strategic view-point, does not guarantee success;

(2) creative thinking of business managers to design strategies is totally inoperative;

(3) no long-term gain;

(4) profit-motive attitude to the exclusion of other objectives; and

(5) coordinating framework necessary for a large organisation is totally lost as lower-level managers get freewheeling of their attitude and shortsightedness.

Yet, freewheeling opportunism finds its relevance to business at times, when and where—

(i) business environment is turbulent (i.e., predictions impossible);

(ii) size of a firm is small (i.e., shops or small traders);.and

(iii) an industry is fashion or sensation-oriented (e.g., video cassettes, discs of songs or news letters).

Q.13. Government, as an element of environment, offers opportunities and poses threats to business. Discuss.

Ans. Government offers opportunities in the following areas (examples only) :

(i) economic planning in key sectors of economy;

(ii) education and training through its institutions (IIT, IIM, etc.), or via grants to councils (e.g., National Productivity Council);

(iii) buying goods and services from, or awarding contracts to, private firms;

(iv) monitoring interest rates and exchange rates;

(v) protecting intellectual property and enforcing laws on industry and commerce;

(vi) providing incentives (e.g., tax holidays, subsidies, duty drawbacks);

(vii) creating entry barriers to foreign business through import tariffs;

(viii) sustaining research and development (e.g., Council of scientific and industrial research, Leather research institute, etc.);

(ix) opening new frontiers of business through privatisation and liberalisation, etc.

Examples of threats (i.e., impediments) posed by the Government may include :

(i) strict regulations on health, safety, environmental pollution;

(ii) grant of discretionary production licences;

(iii) sectional interests taken care of without valid reason;

(iv) price control mechanisms enforced on certain industries;

(v) consumer protection laws;

(vi) fluctuations in indirect taxes causing market distortions;

(vii) undue favour or response to political pressure leading to policy changes, uncertainties, and disruption in stock markets;

(viii) tax raids and arrests of industry giants, etc.

Q.14. Write a brief note on contingency planning.

Ans. Prospects of the future can be classified into certainty, uncertainty and ignorance. Each requires a different type of planning : commitment, contingency, and responsiveness.

Commitment planning can be carried out with respect to those aspects of the future about which one can be virtually certain. In view of the probability of committing mistakes or errors, there is a necessity of continuous updating of estimates.

Even if the future is uncertain, we can assign probabilities of occurrence of certain events. Ackoff defines contingency planning as “the process of planning events when occurrence is uncertain, but assumed in the original plan. The high probability of occurrences and the severe impact once they occur merit forward planning in specifying alternative action and quick regrouping to meet contingencies.”

In this context, Ackoff cites the example of motor power. One really does not know what type of motor power will eventually replace the internal combustion engine in automobiles, but one can be”reasonably sure that it will be either a ‘cleaned up’ engine of the same type or one that is powered by steam or electricity, by a battery or fuel cell. In such cases, contingency planning is required; that is, we should prepare a plan for each eventuality so that we can quickly exploit the opportunities that are presented when the future makes up its mind.” –

It can, thus, be stated that contingency planning applies to both strategic and tactical planning whenever critical assumptions of the original plan are threatened by a high probability of uncertainty.

Since most business decisions are taken under highly uncertain conditions, Chang and Campo-Flores suggest that management should try “to identify and evaluate critical assumptions, to remain alert during the execution of strategy, and to respond quickly and swiftly to contingencies, thus reducing surprises and risks.”

This type of planning finds its extensive use in the military and defence departments.

A contingency plan is a plan to cope with critical developments (e.g., major changes in competition, government policy, strikes, war, natural calamities, etc.) which mark major deviations from the strategic planning.

Contingency planning prevents panic in crisis situations and encourages the managers for quick response to change.