The budget is an expression of the expenditure plan. It is estimated to meet the financial requirements of advertising plans so that advertising objectives with planned strategies may be realised within a given time frame.

It is a statement of proposed advertising expenditure; a guideline for allocating the available funds to the various functions and activities of advertising.

The nature of the advertising budget, advertising appropriation, allocating advertising budget and retail advertising budget are the main decision areas of the advertising budget.

Learn about:-

ADVERTISEMENTS:

1. Meaning of Advertising Budget 2. Nature of Advertising Budget 3. What Should your Advertising Budget Be? 4. Advertising Budget Process

5. Advertising Appropriation. 6. Allocating Advertising Budget 7. Retail Advertising Budget 8. Economics of Advertising and Advertising Budget.

Contents:

- Meaning of Advertising Budget

- Nature of Advertising Budget

- What Should your Advertising Budget Be?

- Advertising Budget Process

- Advertising Appropriation

- Allocating Advertising Budget

- Retail Advertising Budget

- Economics of Advertising and Advertising Budget

What is Advertising Budget: Meaning, Nature, Process, Appropriation, Allocation and Economics

What is Advertising Budget – Meaning

A budget is an expression in monetary terms of the forward plan and the proposed activity. Advertising plan includes, sales targets, product facts, marketing information, competitive situation, creative platform, copy treatment etc. The advertising budget is the translation of an advertising plan into monetary form. It states the amount of proposed advertising expenses and informs the management of the organisation the expected cost of executing the advertising plan.

ADVERTISEMENTS:

The advertising budget should concentrate on the following two aspects:

i. It should be constructed considering the financial strength of the organisation.

ii. Specific operational activities should be identified and detailed allocation of funds should be specified.

The budgetary process should follow the steps listed below:

ADVERTISEMENTS:

i. Preparation of budget

ii. Presentation and approval of the budget

iii. Execution of budget, and

iv. Monitoring and controlling of the budget,

ADVERTISEMENTS:

The advertising manager in consultation with marketing research division and other facilitating agencies prepare the advertising budget. The budget is forwarded to the top management for approval.

Advertising budget is not an exception to the general budget. It is the translation of an advertising plan into money. It includes a large body of information embracing sales goals, product facts, marketing information, competitive situation, creative platforms and rough examples of treatment.

While preparing an advertising budget, the person who is entrusted with this function must observe two fundamentals:

(i) Budget must be constructed with the financial capabilities of the company otherwise the plans set will remain unexecuted due to shortage of funds.

ADVERTISEMENTS:

(ii) It must specially contain the details on the allocation of funds to specific operations.

What is Advertising Budget – Nature

The advertising budget is a plan of expenditure to be incurred on the advertising campaign. The expenditure may be to meet the present expenses as well as future expenditure. Budget decisions explain the budget strategies and programmes. The appropriation is the total amount of the expenditure to be incurred on budgeting. It is a limiting factor in determining the size of the advertising campaign.

The selection of media and messages also depends on the amount of the budgeted expenditure. A moderate budget indicates that neither too little nor too much money will be spent on advertising. The budget may be curtailed by framing a precise message and determining the colour, space and time to be used without hampering the total advertising plan.

The nature of advertising can be explained under:

ADVERTISEMENTS:

1. Advertising as an investment, and

2. The process of the advertising budget.

1. Advertising as an Investment:

Advertising budget is assigned to build the image and reputation of the organisation. The achievement of the budget is observed over a long period. Some of the expenditure on advertising attracts customers immediately; they buy the product when they listen to or view the advertising message. This expenditure is known as revenue expenditure. Some expenditure is incurred on building the image and reputation.

The effects of advertising are realised gradually over a long period. This expenditure is capital expenditure or investment. The expenditure on advertising is accepted as revenue expenditure by the income-tax authorities. The marketing manager is authorised to control and spend the money assigned to him for advertising purposes.

ADVERTISEMENTS:

Advertising expenditure is a capital investment when it is incurred to build the image, goodwill and reputation of product and company; and this results in a gradual increase in the sales, although the expenditure is considered as revenue expenditure in the accounting entry. It is an outlay or expenditure made today to achieve benefits in future. This expenditure is known as capital investment although it is assigned under the revenue budget but it is not accepted as a capital budget.

The advertising expenditure may be increased or decreased, depending on a particular situation. If it is observed that advertising is not yielding satisfactory results, the expenditure is curtailed or not incurred at all thereafter. The costs and benefits of advertising are evaluated periodically to ensure that the budgeted money has been rationally and economically spent.

However, the present returns are not merely a guideline to advertising expenses. The future returns and inflows are properly evaluated to suspend or reject the expenditure. A cut in the advertising budget during a recession may result in the maximum shortfall in sales in subsequent years.

Higher expenditure during recovery may give higher returns in future, although the present returns may be nominal. The expenditure on advertising is made for the present as well as the future returns. It is incurred to stimulate future sales as well as to retain the present market share of the product. Advertising expenditure builds consumer franchise. It is a long-term investment for the building of the image of brands, products and the company.

2. Process of Advertising Budget:

The advertising budget is a statement of the advertising plan in financial terms. It is the allocation of available funds to various advertising functions after determining the total funds available for advertising purposes during a specified period.

The budgetary process involves:

ADVERTISEMENTS:

a. Preparation,

b. Presentation,

c. Execution, and

d. Control.

a. Preparation:

The total expenditure on advertising is estimated on the basis of the information of markets, product, pricing, image, message and media. The determination of the total funds is the first step in budgeting, which is known as budget appropriation. The determination of advertising appropriation depends on the existing sales, the unit of sales, and the expenditure on advertising and affordable capacity.

ADVERTISEMENTS:

After determining the appropriation, the next step is to specify the expenditure to be incurred on each function of advertising. The allocation of appropriation to different advertising activities in made on the basis of the contribution to advertising and the attitude of the management.

Thus, the total budget is cut into small budgets for each advertising function. Advertising budgets are prepared for each market segment, time and geographic area.

b. Presentation:

The budget prepared by the advertising manager is presented to the marketing manager who decides the rationale and the contribution of the budget components. The budget is modified on the basis of the prevailing marketing conditions and management requirements.

The top executive may also fix the budget and budget components. The financial manager is consulted before this decision is taken. The budget is modified in the light of sales forecast, sales opportunities and the role of advertising in capturing the market share. The advertising plan is then formulated for the final budget.

c. Budget Execution:

ADVERTISEMENTS:

The execution of the budget is done through routine activities. The cost of advertising, production, purchase of advertising time and space and other functions are considered. Constant surveillance and periodic checks determine whether the advertising norms are implemented and budgets properly utilised.

The budgets are prepared in the light of the normal marketing conditions. If the conditions change, the budgets are changed accordingly. Contingency funds are provided in the beginning, which are used during times of need.

d. Control of Budget:

The advertising budget should not be less than the advertising expenditure. The expenditure is compared with the provision in the advertising plan. No larger amount should be spent unless the advertiser is constrained to do so in the light of existing conditions. The planned expenditure and the actual expenditure should be on parallel lines.

The budgeted expenditure on advertising should be used only for advertising purposes and not for other purposes. Since sales promotions include several functions other than the advertising function, the advertising budget should be used only for the advertising purposes and not for other sales promotion strategies – that is, on personal selling, merchandising, packaging, public relations, etc.

There should be a separate budget for each sales promotion strategy. When the budget is exhausted by other functions, the phenomenon is known as budget attrition, which should be avoided. There are some combined expenditures on sales promotion which may be drawn from the advertising budget.

What is Advertising Budget – What Should your Advertising Budget Be?

Advertising is the sea of the budget absorption, and therefore, a company should keep a check on the spending for the advertisements. Some critics comment that large consumer-packaged-goods firms overspend on advertising as a form of insurance against not spending enough, and industrial companies underestimate the power of company and product image building and thus, underspend.

ADVERTISEMENTS:

Although, advertising is treated as a current expense, part of it is really an investment in building brand equity and customer loyalty. When a company spends Rs.50 million on capital equipment, it may treat the equipment as a five-year depreciable asset and write-off only one-fifth of the cost in the first year. But, when it spends Rs.50 million on advertising to launch a new product, it writes off the entire cost in the first year, which reduces its reported profit.

A well-planned and realistic advertising budget, keeping in mind its consequent effects on the financial statements of the company, contributed maximum to the effectiveness generated by the advertisement. For this, the company should consider various factors that affect the advertising budget decisions and can emphasis on controlling the same, as appropriate to the company.

The factors influencing advertising budget decisions are explained below:

i. Stage in the Product Life Cycle- New products typically merit large advertising budgets to build awareness and to gain consumer trial. Established brands usually are supported with lower advertising budgets, measured as a ratio to sales.

ii. Market Share and Consumer Base- High market share brands usually require less advertising expenditure as a percentage of sales to maintain share. To build share by increasing market size requires larger expenditures.

ADVERTISEMENTS:

iii. Competition and Clutter- In a market with a large number of competitors and high advertising spending, a brand must advertise more heavily to be heard. Even simple clutter from advertisements, not directly competitive to the brand, creates a need for heavier advertising.

iv. Advertising Frequency- The number of repetitions needed to put across the brand’s message to consumers has an obvious impact on the advertising budget.

v. Product Substitutability- Brands in less-well-differentiated or commodity-like product classes (beer, soft drinks, banks, and airlines) require heavy advertising to establish a differential image.

What is Advertising Budget – Process

1. Collection of Data and Preparation of Budget:

The advertising department is responsible for the planning of advertising work after getting information from various sources. Determining the size of the future advertising appropriation is the first step in preparing the advertising budget. The budget must be allocated among different market segments, time periods and geographical areas depending upon the market potential within that segment, period or area.

2. Presentation and Approval of the Budget:

The next step in the budget making process, after it is developed by the advertising head in consultation with the agency personnel is to present it before the C.E.O for approval.

3. Budget Execution:

The important task undertaken for this purpose is the purchase of authorised time and space over the media and the agency handles the job for and on behalf of advertiser. The costs of advertising production such as making television commercials can also be significant elements in the overall expenditure of advertising.

4. Control of Budget:

It is the duty of advertising manager to see whether actual advertising expenditures coincide with the budgeted expenditure or not.

A procedure must be evolved which brings information about current expenditure to the advertising manager.

Statistical Advertising Budget Model:

One modelling approach concentrates, on determining an optimal total advertising budget without specifically considering creative design or media decisions.

It is a model, which is based on developing a functional relationship between advertising expenditure and some measures of desired market response, usually sales. Information is collected on both sales and advertising expenditures for some previous time period in order to estimate the relationship between the two models are usually of the form –

S = a + b1X1 + b2X2+………. + bnxn + U

Where,

S = Sales of a product or brand

x1 = Advertising expenditures

x2 – xn = Other variables to influence sales

b1 – bn = parameters estimated from data showing the relationship of the corresponding variables to sales

U = Random error

The data analysis shows that a model sufficiently explains sales variations and that advertising is significantly related to sales, it may aid in the budgeting decision. The data for statistical advertising model may be generated in several different ways. Time series data may be used when a firm has kept records of sales, advertising expenditures, and other variables included in the model over enough past periods to provide a sufficient number of data points.

What is Advertising Budget – Appropriation

The term advertising appropriation refers to the total sum of money allocated to advertising during a specified time. It is the way in which this sum of money is allotted, during this period, to different advertising activities. The advertising budget includes advertising appropriation and allocation.

The factors influencing advertising appropriation may be advertising plans, marketing opportunities, production costs of advertising etc. The appropriation is determined by using several formulas, such as – affordable approach, sales approach, and competition approach and so on.

Thus, the advertising appropriation takes into account:

1. The factors influencing appropriation, and

2. Determination of appropriation.

1. Factors Influencing Appropriation:

The factors influencing budget appropriation are:

a. Advertising plans,

b. Marketing opportunities,

c. Competition,

d. Product life cycle,

e. Cost of advertising,

f. Type of the product and

g. Importance of the retailer.

a. Advertising Plans:

The advertising objectives, strategies and programmes determine the total amount of expenditure to be incurred by the company for advertising purposes. The internal as well as external opportunities are evaluated for the appropriation. The objectives refer to advertising opportunities which can be exploited by the company.

Depressed economic climate and intense competitive activity call for a larger outlay on advertising. The implementation of sophisticated strategies requires more money for the purpose. Adequate money should be provided for the implementation of the routine programme of advertising.

b. Marketing Opportunities:

Marketing opportunities determine the amount of appropriation. Advertising should exploit the potential of the market. The characteristic of consumers and their respective requirements would suggest the total amount of funds to be utilised by the company. Marketing opportunities are different in different markets, so the quantum of advertising appropriation has to be differently determined to arrive at the total amount to be budgeted.

Seasonal demand advertising triggers a longer expenditure than the off-season demands. The market may be regularised by off-season discounts and sales promotion for which advertisements are given in newspapers, television, radio, etc. Product opportunities are also taken into account while determining market opportunities.

The strategies of emotional appeal fear appeal and other factors determine the size of funds to be allocated to exploit existing as well as potential marketing opportunities.

c. Competition:

The nature and pressure of competition influence the size of the appropriation. A greater intensity of competition may call for larger funds for advertising. Competitive advertising helps expand demand. Domination of media or markets by the competition may call for larger funds.

The cost and efficiency of each medium are the fundamental determinants of the size of the appropriation. Competitive advertising is used to meet competition. An imaginative advertising theme and the unique selling proposition may perform suitable jobs for competitive advertising.

d. Product Life Cycle:

The product life cycle is also an important determinant of the size of the total budget Consumer awareness and increased usage are taken into account to determine the level of advertising and costs. A knowledge of the life cycle of several products of the company is helpful in determining the size of the appropriation and the budget.

The need for advertising decreases as the age of the product increases. It is possible to rejuvenate the product by injecting more funds to build its image. Efforts should be made to know which life cycle demands how much funds for advertising so that the total appropriation may be finally approved by the management.

e. Costs of Advertising:

The total costs of advertising are decided for appropriation. The advertising costs include the expenses incurred on developing and preparing advertisements, designing the message and selecting the media. The fees for action, direction, the costs of building sets and travelling to locations, tape recording and visual cassette recording, expenses on print media and broadcast media, etc., are included in the costs of advertising.

The costs of advertising also include administrative expenses, salaries, costs of resources used, and fees to outside bodies and institutions. Contingency funds are also included in the costs of advertising.

f. Type of Product:

The type of product to be marketed determines the size of the appropriation. Consumer products require a larger advertising budget than industrial products. If the opportunities for product differentiation are substantial, the returns on advertising will be higher than those on undifferentiated products.

The hidden qualities of the product and brand are the guiding factors in the selection of the media. The absence of price competition may reduce advertising costs. People pay a higher price for a brand that satisfies them the most. Advertising is more effective in non-price competition and less effective in a price competition situation. People purchase those items which are heavily advertised. Primary products need more advertising.

g. Retailing:

Advertising will be less in demand if retailing is co-operative and effective. If retailers do not communicate product attributes to consumers, advertising becomes essential. Advertising and retailing create a demand for the product in the market.

2. Determination of Appropriation:

The appropriation for advertising may be determined on the basis of:

a. The affordable approach,

b. Competitive parity,

c. Percentage of sales,

d. Unit of sales,

e. Objectives and tasks,

f. Marginal approach, and

g. Mathematical models.

a. Affordable Approach:

Affordable approach means that advertising will be appropriated after all the other unavoidable investments and expenses have been allocated. The appropriation is set simply on the basis of an assessment of what the company can afford for advertising purposes during the period of the operation of the budget.

It is an arbitrary method, but it limits the maximum expenditure to be incurred on advertising. This is the decision of the management, which is based on past experience. The goals and aggressive methods of advertising are considered for appropriation purposes. The management may decide to spend 20 per cent or 10 per cent of liquid assets for advertising purposes.

If it is very conservative, the budget may be low. Some managers use the go-for-broke method, whereby every month, the advertising budget is expanded by a certain percentage or amount For example, if it is decided that Rs. 5000 should be added every month to the basic advertisement expenditure of Rs. 1,00,000, this would be an acceptable proportion if the sales are increased by Rs. 5000 or more per month. If the sales do not increase proportionately, the additional expenditure should not be incurred at all.

The affordable approach does not encourage long-term planning. The affordable amount cannot be predicted easily. The short-term objectives are overlooked. If the sales decline, the size of the budget may be reduced. This may not prevent the emergence of the laggard situation. It is, therefore, not a logical or quantifiable approach. However, the affordable approach on the basis of the experiences of the management is often adopted by the planner.

b. Competitive Parity:

The producer tries to establish parity with the competitors. So he formulates such types of budget as would be equal to the budgets of the competitors. The competitive parity method has the advantage of recognising the importance of competition in advertising. Imitating the competitor’s budget is not productive because it ignores the objectives, strategies and programmes of the producers.

The level of production and marketing have a significant bearing on the budgeting process, but the competitive parity ignores it. The competitive parity is used to maintain the collective wisdom of the industry. It minimises aggressive action and advertising wars.

This approach is acceptable as rational because the budget is decided in the same market conditions, for the same opportunities, pursuing the same goals, having the same reputation, allocating the funds in the same way in the same media, and because the company is operating in the same manner.

It is not always feasible because competitors keep their plans secret. There may be an unwise allocation of money. The imitator may be unable to afford the budget of the competitors.

c. Percentage of Sales:

The percentage-of-sales method is more popular than the other methods. A pre-determined percentage of sales value is earmarked for advertising purposes. The percentage remains constant. The previous year’s sales are taken as the yardstick for the allocation of the budget.

The main advantage of this method is its simplicity. The budget varies with what the firm can afford on the basis of its sales. Suppose, it is decided that one per cent of the sales will be allocated to advertising; the advertising budget will then increase or decrease in proportion to the rise or fall in sales.

The quantum of sales determines the financial capacity of the firm. Competitive stability may also emerge, for the expenditure is directly related to the funds available on the basis of sales.

The procedure is illogical because it assumes that advertising is a result of sales rather than a cause. It is not very flexible because it does not allow for extensive advertising when the need for advertising increases because of a fall in sales. The company does not take advantage of sales opportunities.

The sales may increase rapidly if advertising is adequate during the innovation-stage or rising potential. But there is a large variation in the productivity of advertising at different levels of sales. The return on advertising may diminish after a certain stage, although this approach permits a bigger size of the budget at higher sales.

The company may, therefore, underspend when the potential is great and overspend when the potential is low. Since the funds made available will vary in proportion to sales, there is a limited scope for long-term planning of advertising expenditure. Moreover, it does not take into account the changing goals of the company and the market conditions. Short-term and long-term opportunities are overlooked.

The size of the budged may be determined on the basis of opportunities, i.e., anticipated future sales. This is also logical because the budgeting process precedes the sales. Advertising is not the only factor stimulating the sales. The sales forecast technique is used for the purpose of evaluating future sales opportunities. The economic and market conditions are evaluated to forecast these opportunities. The past and future sales are averaged to stabilise this approach.

d. Unit of Sale:

The unit of sale determines the size of budget. A fixed amount per unit is allocated for advertising purposes. If Rs. 1,000 per vehicle is assigned to advertising, the budgeted amount will be Rs. 100,000 for 100 vehicles. The unit of sale is the basis of budgeting for durable goods and industrial goods. The units of forecast sales are the basis of appropriation.

The unit-of-sale method is applied easily and for a sufficiently long period, it can give the advertiser reasonably accurate predictions of the advertising-to-sales ratios. The advantages and disadvantages of the percentage sales approach are also the advantages and disadvantages of the unit-of-sale approach. It is, therefore, inflexible and illogical.

e. Objectives and Task Approach:

The term objectives and task approach refers to the cost of achieving the objectives by applying the appropriate task. The advertising objectives are established. The number of insertions needed for achieving the objectives after selecting the media is estimated and the cost of the media programme is calculated.

The cost per medium is estimated to arrive at the total cost of advertising. The relationship between costs and objectives is determined. The costs are examined on the affordable and benefits grounds. The costs of advertising are estimated accordingly.

The objectives of advertising are determined after a thorough evaluation of the internal and external environment. After defining the objectives in terms of sales, profits, and promotion, the cost of achieving them are estimated. If the cost of advertising works out to be higher than the affordable funds, the cost is curtailed or the objectives lowered.

Sometimes, the percentage-of-sales method is used for cost determination in advertising. The sale is a specification of objectives. Some authors have suggested that sufficient advertising should be done for two or three years to produce an adequate sales-return.

f. Marginal Approach:

The cost-and-benefit analysis offers the basis of budgeting and the costs of advertising. The marginal contribution of each unit of each media is a guiding factor in estimating the cost per unit. The aggregation of these costs of units is taken as the total cost of advertising. The cost of advertising should be at least equal to its benefits. An economic and marginal analysis is made to arrive at the optimum level.

The marginal costs and marginal benefits should be equal in determining the optimum level of advertising. The-total cost is decided at that point Benefits are determined on the basis of sales. If these factors are estimated, this approach may provide a rational solution not only for determining the size of the appropriation, but also for the allocation of funds in the budget.

g. Mathematical Models:

Mathematical models have been developed for advertising appropriations to attain the objectives and tasks of advertising and to measure the level of success that has been achieved by the advertiser. Mathematical models have been successful for determining the size of the advertising appropriation.

The advertising objectives within the periphery of marketing objectives are set. The tasks to achieve the advertising objectives are determined on that basis. The appropriation is fixed to attain them effectively and economically. An optimal budget is developed when the total cost of advertising does not exceed the additional profit derived from it.

Some authors have used mathematical models to arrive at the total amount required for advertising purposes. The important models are – sales response and decay models, communication-stage models, adaptive-control models, competitive-share models.

I. Sales Response and Decay Models:

The sales-response-and-decay models set out a measure to shape the advertising sales-response function with a view to determining mathematically how much advertising is needed for profit. It establishes a relationship between advertising expenditure and sales. The future budget is determined on the basis of this relationship.

The sales-response to advertising is developed in the form of a curve to find out the relationship at a particular point. The relationship indicates three stages- sales response constant, sales decay constant and the saturation level of sales.

i. Sales Response Constant:

The sales response constant relationship represents the sales revenue generated by one unit of advertising expenditure when sales are zero. For example, if a firm having no sales spends Rs. 1,000 on advertising in one month and if this results in sales of Rs. 5,000, the sales response constant will be 5, i.e., Rs. 1.0 spent on advertising yields a sale of Rs. 5.00.

ii. The Sales Decay Constant:

The sales decay constant relationship is used to describe the behaviour of sales revenue in the absence of advertising. If a company stops advertising, the sales will decline. The competitors will lure away all the customers of the company. Gradually, consumers will forget the brand and sale may go down to a very low level.

iii. The Saturation Level of Sales:

The saturation level of sales represents the level of sales which is unlikely to be surpassed, irrespective of the level of advertising.

This level gives the following relationship:

![]()

Where,

δ s – stands for change in sale.

δ t – stands for change in time.

r – stands for the sales response constant, i.e., the proportion of sales generated per advertising at zero level of sale.

A – stands for the rate of advertising expenditure at the time.

M – stands for the saturation level of sales, i.e., the maximum that can profitably be achieved by means of the advertising campaign.

S – stands for the rate of sales at the time.

λ – stands for the sales decay constant, i.e., the proportion of sales lost in each time period when advertising is reduced to zero.

This model suggests that the change in the rate of sales in time t will be the effect of advertising, sales response constant and the sales decay constant. To achieve a high sales rate, larger advertising is required, provided that the sales response and sales decay are constant.

The advertising effect will also vary with the change in the saturation level of sales, response constant and sales decay constant. This model is also used to determine the amount of advertising required to achieve a specified rate of growth in sales.

This model is criticised on the ground that the sales response constant, the sales decay constant and saturation level are difficult to calculate. The company’s sales response to advertising is a function of six factors, i.e., percentage of loyal consumers; no loyal consumers; relative roles of price, distribution, advertising and product characteristics; the relative roles of the interaction of the product and advertising; the relative amount and value of the company’s advertising appropriation; and the size of market.

II. Communication Stage Models:

In the communication stage model, the logic is the money spent on advertising media process, the gross impressions on a target market which results in awareness, interest and desire leading ultimately to sale. It arrives at the appropriation by observing the effects of the budget on the variables that link advertising expenditure to sales.

The market-share goal is developed first to calculate the size of the market that might reasonably be expected to be reached by advertising. The size of the market that may try the product is also calculated to estimate the number of advertising per exposure or trial. The gross rating points (GRP) are also calculated to estimate the appropriation necessary on the basis of the average cost per GRP. The communication stage model incorporates the objectives and tasks to be realised. The calculation at every stage is a difficult task.

III. Adaptive-Control Models:

The adaptive-control models assume that the advertising sales-response function is not sufficiently stable over a long period of time to be used for predictive purposes. The response function is influenced by such factors as economic conditions, product design, competitive activity and advertising copy.

This model experiments with each factor for a period. The advertiser can get estimates of sales response for each stage and update his advertising budget accordingly. The costs for influencing these factors are estimated to arrive at the size of the appropriation.

IV. Competitive-Share Model:

The competitor’s activities and market share are plugged into a decision situation. The competitors’ reactions are calculated to determine the size of the appropriation. The probable reactions of competitors are evaluated. The principle of the game theory has been used to evaluate competitive reactions and strategies.

The model is straightforward and requires a matrix with the strategies open to the producer, on the one hand and the possible reactions of the competitor, on the other. Probabilities of outcome are assigned to each combination of strategies. The producer takes advantage of the weaknesses of the competitor.

The game theory is known as the fundamental theorem of market-share determination. According to it, an equivalent share of profit is to be spent to acquire a similar market-share. Competitive share determination and interaction are a very dynamic phenomenon.

The actions and reactions of competitors are recorded at each stage of the advertising campaign. The competitor may retaliate by maintaining his expenditure on advertising at a constant level, increasing the size of the sales force, reducing the price and engaging in an intensive sales promotion campaign.

What is Advertising Budget – Allocation

The next step in fixing the advertising budget is the allocation of appropriation to different tasks and media of advertising. The avenues of budget-utilisation are determined for an effective and economical use of the expenditure. The advertising process is broken into several units and each unit is assigned adequate funds for completion of the task.

The size of the allocated funds is revised from time to time to find out their effectiveness. The revision process begins at the bottom of the activity to find out whether the size of the budget is adequate or inadequate. The advertising budget is allocated according to objectives, the media used, the message transmitted and the geographic regions to be covered.

1. Allocation by Objectives:

Advertising objectives have been useful guidelines to the allocation of funds. The objectives are broken down into campaign objectives. The month, year and other time factors are the basis of campaign objectives. Funds are allocated to meet each campaign objectives. The length of the campaign determines the amount of funds required. Media goals and other short-term functions are determined.

The results of previous advertising objectives determine the level of funds required for the purpose. The objectives of media, message and competitive approach determine the size of the appropriate funds required to meet the tasks. The advertising objectives are revised and supporting budgets are allocated for each component of the objective.

Appropriate and experimental campaigns are formulated and the cost per campaign is determined. Some contingency reserve funds are set apart to meet any unforeseen requirements of the campaign. The campaigns with budgeted funds are submitted to the marketing management which determines the size of the budget for each campaign.

If, in its opinion, the budget is higher, it is pruned for each campaign or the campaign itself is curtailed by the management. The allocation process continues to determine the budget for each component of the objectives of the advertiser.

2. Allocation by Media:

The budget appropriation is allocated amongst the different media according to their contribution, the administrative overheads, media copy development and reproduction, and research. The media require significant funds for coverage, generally 80 per cent of the total budget which is allocated to the media.

Of the several media, television accounts for about 60 per cent of the total budget. Small firms spend more money on newspaper and magazine advertising. They spend about 90 per cent of their budget on the print media. Some tiny industries may spend 100 per cent only on vehicles and loudspeaker announcements. The allocation depends on the industry, the size, needs and objectives of each firm.

Reach, frequency and continuity also determine the size of the funds required. Media objectives are met with the allocation process.

The budget is allocated according to the message developed for each media. The copy development and research functions require specific amounts. Message development is divided into layout, design and illustration. The marginal contribution of each message and copy determines the maximum amount of expenditure to be incurred on them.

The probability of expenditure and the contribution of each copy are compared to determine the actual amount of budget for each copy. The budget becomes the control mechanism of expenditure. A comparison of several years’ budgets shows how much is to be spent and how much expenditure should be curtailed with a view to economical and effective utilisation of funds.

The market is divided into several segments. The development of each segment requires allocation of funds. The management decides how much money should be spent on a particular market segment. The push or pull theory is used for distribution purposes. According to the push theory, the development of middlemen in the channel at distribution is essential.

The longer the distribution-channel, the higher the cost of advertising. The contribution of each component of the channel is assessed before advertising at the cost-and-budget decision. The pull theory lays emphasis on the need for communication with the final user of the product.

The users may be heavy users, light users, opinion leaders, innovators, followers and late adopters. Each product stage is identified and an adequate amount of budget is allocated for success at every stage. The contribution of every component of the channel determines the amount of appropriation to be allocated to each.

The budget is generally allocated on the basis of the sales of each product line. If the manufacturer is producing different articles, the budget is allocated on the basis of the value of sales of each article.

The stage of product life cycle, the amount of competition, the product faces, the extent of market penetration, the margin contributions of each product and the role of advertising for their development – these are the deciding factors in budget allocation. A product contributing a significantly higher share of the profit is allocated larger funds. A product in the initial stage of marketing requires a larger advertising budget than the product in its maturity stage.

6. Allocation by Geographical Area:

Budget is allocated according to the geographical area covered by advertising. To some areas, larger budgeted funds are assigned to harness the potential marketing opportunities. Advertising in local newspapers and magazines receives larger funds than advertising in the national print media to exploit the local marketing opportunities.

In some markets, sustained spending is essential to prevent deterioration in the brand’s competitive position. Larger funds are allocated to develop a poor market and a smaller amount is allocated to highly developed markets. Where trading is controlled by middlemen and retailers, a smaller budget is required for advertising purposes.

What is Advertising Budget – Retail Advertising Budget

The advertising budget prepared by a retail store is known as the retail advertising budget The problems and the process of budgeting of the retail store are the same as those of the manufacturer. The head of the retail store is involved intimately in budgetary matters of all kinds.

The difference between a retail advertising budget and the manufacturer’s advertising budget is only of size. Advertising plays the same role in a retail store as in a manufacturing concern. But efficient handling of advertising funds is more crucial in retail budgeting. Many retailers use advertising for sales expansion.

The retail advertising budget is a part of publicity budget in a retail store, as the advertising budget is a part of the marketing budget of the manufacturer. Publicity for retail store is a wider term which includes advertising, point-of-purchase, display, etc. Retail advertising is divided into institutional advertising and promotional advertising.

Institutional advertising is designed to establish the store as a place of selling. Promotional advertising appeals for direct action. Pricing is important for promotional purposes. Institutional advertising is concerned with the reputation of the store, with style leadership, quality merchandise and services.

The retail store decides how much institutional and how much promotional advertising will be effective for its purpose. The retail advertising budget covers display, point-of-purchase, reputation, publicity expenditure, services and quality merchandise.

It has been analysed here under the:

1. Factors influencing retail advertising, and

2. Retail budget-making process.

1. Factors Influencing Retail Budgeting:

The factors influencing retail budgeting are those which influence the budgeting process of the manufacturer. They may relate to age, location, merchandising, competition, media, area, type of product and support from the manufacturer. A new store spends more on advertising than an established store to win the confidence of customers.

A store located in the centre of the market place needs more advertising to attract people. The promotional stores depend on price cutting. Fashion and dress stores undertake more advertising to attract customers. Retailers need more advertising. A multi-media town draws a larger public.

Advertising is essential for furniture and jewelry stores. If a retailer is an exclusive dealer for one or more brands and if the brand advertisers promote it, there will be need of retail advertising. The manufacturers help retailers in advertising their product If such facilities are available to the retailer, he need not undertake extensive advertising.

2. Retail Budget-Making Process:

Under the retail budget sales goals are set the quality and extent of advertising are determined for promotional purposes and a schedule is proposed for day-to-day advertising.

a. Goals:

Setting the goals and tasks of advertising is the starting point of the advertising programme. Each task or objective is expressed in terms of sales volume. The retailer is urged to start with the previous year’s sales.

Store expansion, increased population, higher income, greater employment, competitive activities, product diversification, etc., are the several factors which are considered in retail advertising. The amount of expenditure on each task and objective is decided and aggregated to arrive at the final amount of the budget for retail advertising.

b. Quantity of Advertising:

The amount of advertising is fixed to fit the sales goal. Competitive advertising should be taken as the base of retail advertising. The retailer may fix the amount of the budget as a percentage of his sales. Several other factors, such as store location, length of time, local reputation, competition, etc., influence the quantity of advertising and the outlay on it

c. Promotional Avenue:

The total budget is divided into various departmental budgets. The retailer predicts the requirements and needs of the customers. He organises advertising in the light of consumer behaviour. Sales opportunities are evaluated and advertising campaigns arc developed accordingly.

d. Budget Schedule:

The advertising budget is scheduled according to the, time available and the market season. A monthly schedule may be proposed for an effective utilisation of the budget. A step-by-step advertising budget is framed and used to popularise the products.

What is Advertising Budget – Economics of Advertising and Advertising Budget

The firm’s purpose in advertising is to increase the demand for its product. The question is often addressed as to how much should be spent on advertising by a profit -maximising firm?

The answer should be that one should follow the golden rule of profit maximisation which states that keep spending until marginal cost equals marginal revenue.

Advertising spending is considered like a factor of production and it has a marginal product, the change in the quantity demanded per thousand rupees of advertising spending.

The problem with the above marginal revenue-marginal cost based analysis is that it is static. It fails to recognise that advertising production function is dynamic. The effect on demand of a given rate of advertising spending tends to increase over the course of some periods.

What is known is that in some industries a good deal of advertising takes place, while in others there is very little.

There are manifestations of the-culture of an industry. If its rivals advertise, firms feels compelled to advertise, as well.

Thus advertising budgets are related to the firm’s perception of the previous year’s advertising spending of its principal rivals.

In developing an advertising plan, objective setting is important and may be significantly influenced by the limitations of the budget. Irrespective of whether a company is multinational, a large company or a medium size company, budget decisions are critical as the money spent on advertising may mean the difference between success and failure.

Budget allocated to advertising is considered as, expense, cutting into profits, rather than an investment. For this reason, when a firm faces rough times, the axe falls on advertising expenditures.

According to economic marginal analysis the assumptions are:

(i) Sales are a direct result of advertising expenditures and this effect can be measured accurately.

(ii) Advertising is solely responsible for sale.

In most cases, it is difficult to find out the direct effects of advertising on sales. According to an expert’s opinion, “Looking for relationship between advertising and sales is somewhat worse than looking for a needle in a hay-stack”.

Instead, it is logical to determine the impact of ad expenditures on the accomplishments of the communication objectives such as awareness, interest, attitude change etc.

Because of the difficulties associated with economic marginal analysis in determining the effect of advertising on sales and revenues, it is rarely used as a basis to allocate advertising budget.

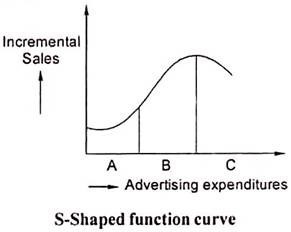

Many advertising and sales promotion, managers subscribe to the S-shaped response function.

According to this model, initial expenditures on advertising have very little influence on sales (A) in the diagram given below –

After a certain budget level has been spent, advertising efforts start having effect and from here on increments in advertising expenditures lead to increased sales (B).

These sales gains continue only upto a point and after that there are little or no gains with additional expenditures (C).

This S-Shaped model suggests that very small advertising budgets are unlikely to have any meaningful impact on sales and also huge advertising expenditures do not necessarily mean definite incremental sales.

The above curve suggests advertisers would attempt to operate with expenditures in the area of rising curves where maximum return on monetary expenditures can be accomplished.